Home

ReportReport

ReportReportThe global IVF Devices and Consumables market is projecting a significant surge to $16.08 billion by 2033. Driven by rising infertility and tech innovations, the analysis covers regional shifts, product segments, and emerging trends, highlighting the industry’s evolution alongside the growing Smart Fertility Tracker Market

The global landscape for reproductive health is undergoing a radical transformation, driven by a combination of technological breakthroughs and shifting demographic trends. At the heart of this evolution is the IVF Devices and Consumables market, which provides the essential tools and media required for assisted reproductive technologies (ART). As more individuals and couples seek professional intervention for infertility, this market has moved from a niche medical sector to a multi-billion-dollar global industry. This shift is often preceded by consumer interest in the Smart Fertility Tracker Market, as individuals utilise early-stage monitoring before transitioning to clinical IVF procedures.

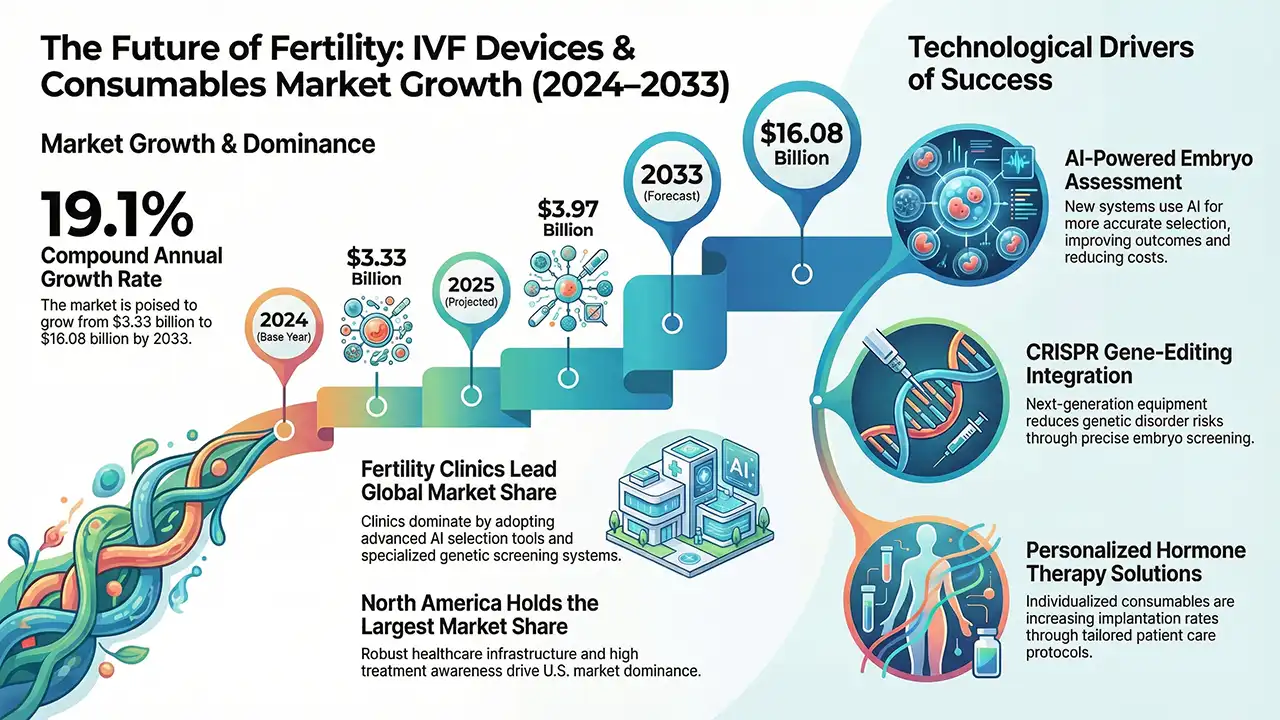

According to recent market analysis, the global IVF Devices and Consumables market was valued at USD 3.33 Billion in 2024. The industry is positioned for an aggressive upward trajectory, with its value expected to rise to USD 3.97 Billion in 2025. Looking further into the forecast period of 2026–2033, the market is poised to reach a staggering USD 16.08 Billion by 2033.

This growth represents a compound annual growth rate (CAGR) of 19.1% during the forecast window. Such a high growth rate is attributed to the increasing global acceptance of ART, advancements in genetic screening, and the expansion of healthcare infrastructure in emerging economies. The integration of clinical solutions with the data-driven insights from the Smart Fertility Tracker Market has also helped in identifying patient needs earlier, streamlining the path to IVF.

The demand for IVF devices and consumables is fuelled by several intersecting factors. Chief among these is the rising prevalence of infertility worldwide, which is heavily influenced by lifestyle changes, environmental factors, and a widespread trend toward delayed pregnancies. As the average age of first-time parents increases, the biological need for assisted conception grows, directly impacting the volume of IVF cycles performed annually.

Furthermore, societal shifts have broadened the patient base for these technologies. There is an increasing desire for IVF services among single parents and LGBTQ+ couples, alongside an ageing population that is more frequently turning to reproductive science. These shifts have moved IVF into the mainstream healthcare system, where it is no longer viewed as a last resort but as a standard medical solution. The preliminary use of tools within the Smart Fertility Tracker Market often serves as the first step for these diverse groups to understand their reproductive health before engaging with specialised clinics.

Technology remains a critical driver of market success rates and, consequently, market size. Recent advancements in IVF equipment, including high-precision incubators, embryo culture systems, and advanced imaging devices, have significantly improved the outcomes of fertility treatments.

One of the most transformative shifts in the market is the integration of Artificial Intelligence (AI). AI-powered systems are now being used for more accurate embryo selection and assessment, which increases the likelihood of a successful pregnancy per cycle. This not only improves patient satisfaction but also reduces the overall cost per successful birth, making the treatment accessible to a wider demographic.

Additionally, breakthroughs in genetic screening and gene-editing technologies, such as CRISPR, are being researched to reduce the risk of genetic disorders in embryos. This push toward safer and more effective treatments is meeting a global demand for precision medicine. Enhanced culture media and individualised hormone therapy solutions are further tailoring the IVF process to specific patient needs, moving the industry toward a model of personalised reproductive care.

The market is divided into three primary product segments: Instruments, Accessories and Disposables and Reagents and Media.

The market is further segmented by technology into Fresh Embryo IVF, Frozen Embryo IVF, and Donor Egg IVF. The shift toward frozen embryo transfers has gained momentum as cryopreservation technologies improve, allowing for better timing of the implantation process and often higher success rates in specific patient groups.

North America, led predominantly by the United States, holds the largest market share. This dominance is underpinned by a robust healthcare structure, high awareness regarding fertility options, and early access to the latest IVF technologies. Ongoing investments in research and development, coupled with increasing insurance coverage for fertility treatments, ensure that this region remains a central hub for the IVF industry.

Europe stands as the fastest-growing region for the IVF devices and consumables market. Countries like the UK, Germany, and France are leading this charge through favourable government policies and healthcare reimbursement models. In the UK, for instance, the National Health Service (NHS) provides partial reimbursement for IVF costs, which has significantly fuelled the dominance and accessibility of these treatments.

The Asia-Pacific region is experiencing rapid growth due to increasing fertility awareness and rising disposable incomes. China, India, and Japan are at the forefront, supported by government initiatives and a burgeoning middle class that is increasingly willing to invest in advanced reproductive technologies. The rise of fertility clinics and the social acceptance of ART in these countries are major contributors to the regional forecast.

The Middle East, Africa, and Latin America are also expanding their market footprints. In the MEA region, countries like the UAE and Saudi Arabia are seeing growth driven by medical tourism and improved healthcare facilities. In Latin America, Brazil and Argentina are emerging as leaders as they improve their healthcare infrastructure and government initiatives aimed at providing fertility services expand.

Despite the robust growth forecast, the market faces significant hurdles. Ethical and social concerns regarding embryo handling and genetic screening remain a primary restraint, particularly in more conservative regions. These concerns can lead to varying levels of societal acceptance and affect the local demand for advanced ART solutions.

Strict regulatory challenges also play a major role. Requirements for the approval of new IVF devices and consumables can be stringent and vary significantly by country. These regulations can delay product launches and increase the cost of production, posing a challenge for manufacturers looking to standardise their offerings across global markets.

The future of the IVF Devices and Consumables market is defined by a shift toward personalised medicine. By tailoring treatments to an individual’s genetic profile, clinics can minimise the number of required cycles and improve success rates, ultimately making the process more cost-effective.

The expansion into emerging markets will continue to be a primary growth driver, as healthcare accessibility improves and the middle class grows in Asia and Latin America. The synergy between clinical IVF and the Smart Fertility Tracker Market will likely deepen, as data from consumer-grade trackers becomes increasingly useful for clinicians in designing optimised, individual treatment protocols.

In conclusion, with a projected value of USD 16.08 Billion by 2033, the IVF Devices and Consumables market is set for a decade of profound innovation and expansion. Driven by technology and a growing global need, the industry will continue to evolve, offering more precise, accessible, and successful options for those seeking to build families.

The University of Aberdeen has launched a redesigned, free IVF success calculator, the OPIS tool, powered by updated national HFEA data. Built with patients at its centre, the IVF success calculator provides tailored success estimates across up to six IVF or ICSI cycles, helping couples plan emotionally, physically, and financially.

A retrospective cross-sectional study of 276 ART patients suggests that the oestradiol-to-oocyte ratio (EOR) could serve as a meaningful prognostic marker for IVF outcomes in PMOS. The research examines EOR across four categories, incorporating subgroup analysis by luteinising hormone activity during ovarian stimulation.

AutoIVF's OvaReady device is advancing IVF egg retrieval technology by recovering "stealth oocytes" from discarded follicular fluid. With Northeastern University co-op students Tori Christianson and Jake Percival refining its prototypes, the Natick, Mass, based startup is preparing for clinical trials, aiming for FDA clearance to improve IVF success rates.

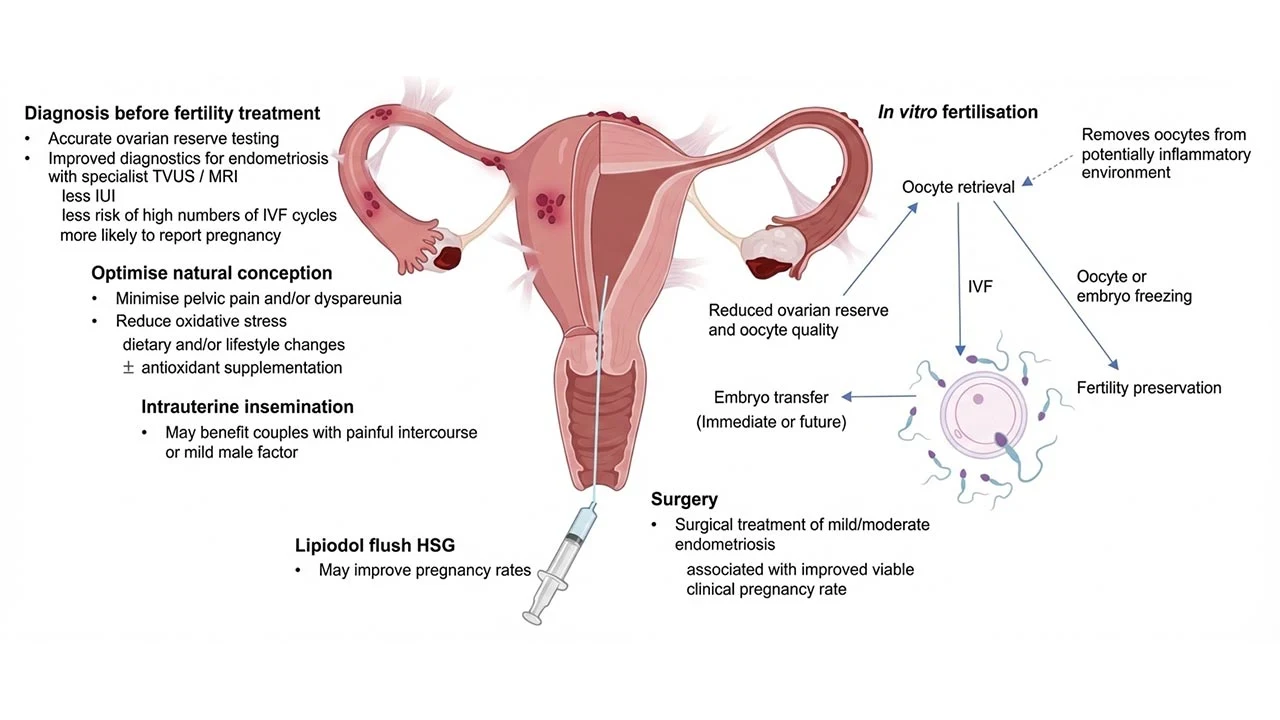

Integrating IVF and Surgical Management in Endometriosis offers a patient-centered strategy to improve fertility while managing chronic pain. By integrating laparoscopic surgery, ovarian reserve assessment, and assisted reproductive technology, clinicians can tailor treatment plans, enhance live birth rates, and optimize reproductive outcomes for women facing complex endometriosis-related infertility challenges.

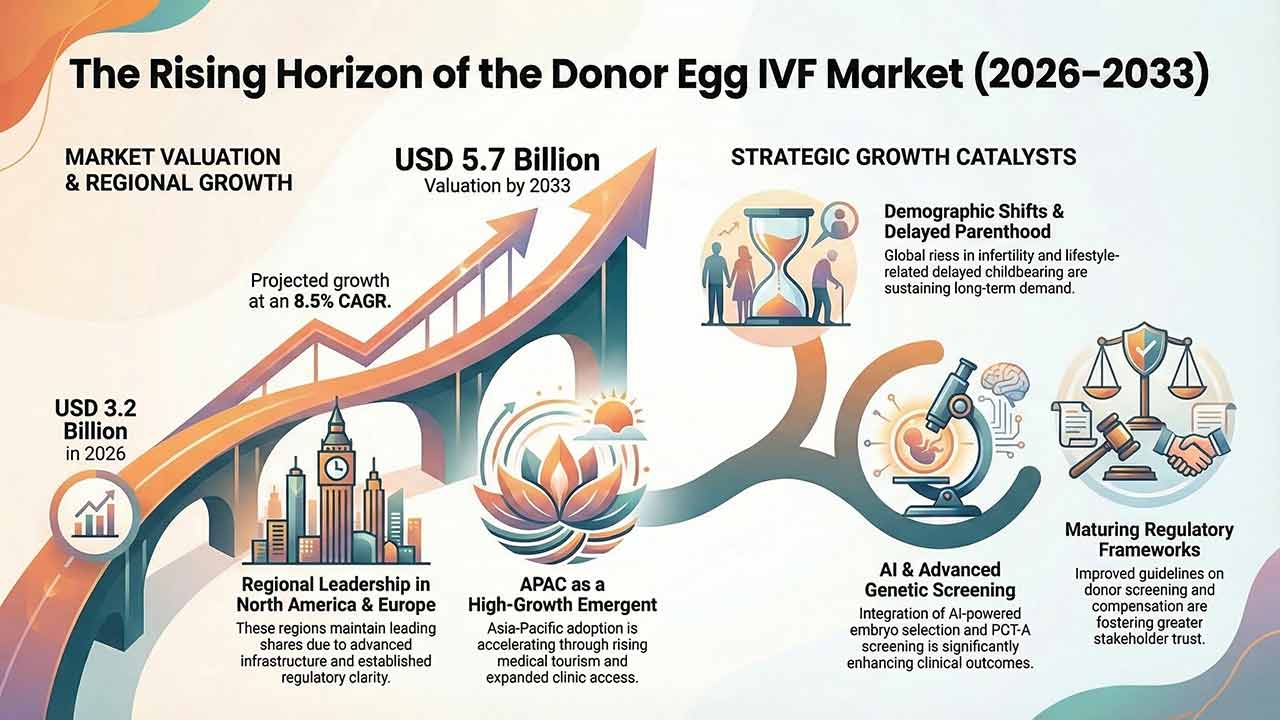

This comprehensive analysis examines the global Donor Egg IVF market, forecasting a valuation of USD 5.7 billion by 2033. The report explores critical growth drivers, including delayed parenthood, technological breakthroughs in embryo selection, and shifting regulatory landscapes, offering a detailed breakdown of market segmentation and regional growth trajectories for the next decade.

Global Preimplantation genetic testing market outlook covering growth drivers, segmentation, regional trends, key technologies, restraints, opportunities, and competitive landscape approaching $1B by 2032.