Home

ReportReport

ReportReportMarket analysis of the infertility drugs market, highlighting the dominance of gonadotropins, online pharmacies as key channels, the competitive landscape, and regional trends, with insights and infographics for 2025-2032.

The infertility drugs market is projected to reach USD 6.36 billion by 2032, with a prominent role for gonadotropins and a surge in online pharmacy channels. Market dynamics, growth drivers, segment trends, and regional and competitive insights are presented below.

Overview and Market Dynamics

Overview and Market DynamicsThe global infertility drugs market was valued at USD 3.98 billion in 2024 and is forecast to achieve USD 6.36 billion by 2032, at a CAGR of 6.03% between 2025 and 2032. The U.S. alone accounted for USD 1.21 billion in 2024, reflecting significant regional relevance. Key growth drivers include rising global infertility rates (impacting over 17.5% of adults), lifestyle changes, delayed childbirth, and advancements in assisted reproductive technologies. Greater awareness, educational programs, and improved at-home access via telehealth and e-pharmacies are elevating market momentum.

By Distribution Channel

By Distribution ChannelBoth established pharmaceutical firms and emerging biotech companies are shaping the competitive field through strategic partnerships, geographic expansion, and broader pipelines. Treatment efficacy, patient time-to-conception improvements, and innovative delivery methods are central competitive factors.

The infertility drugs market is entering an era defined by data-driven personalization, digital access, and innovation. Key factors set to shape its trajectory through 2032 include the success of gonadotropins, expansion of online pharmacies, regulatory shifts, and ongoing investment in R&D for next-generation therapies and delivery technologies.

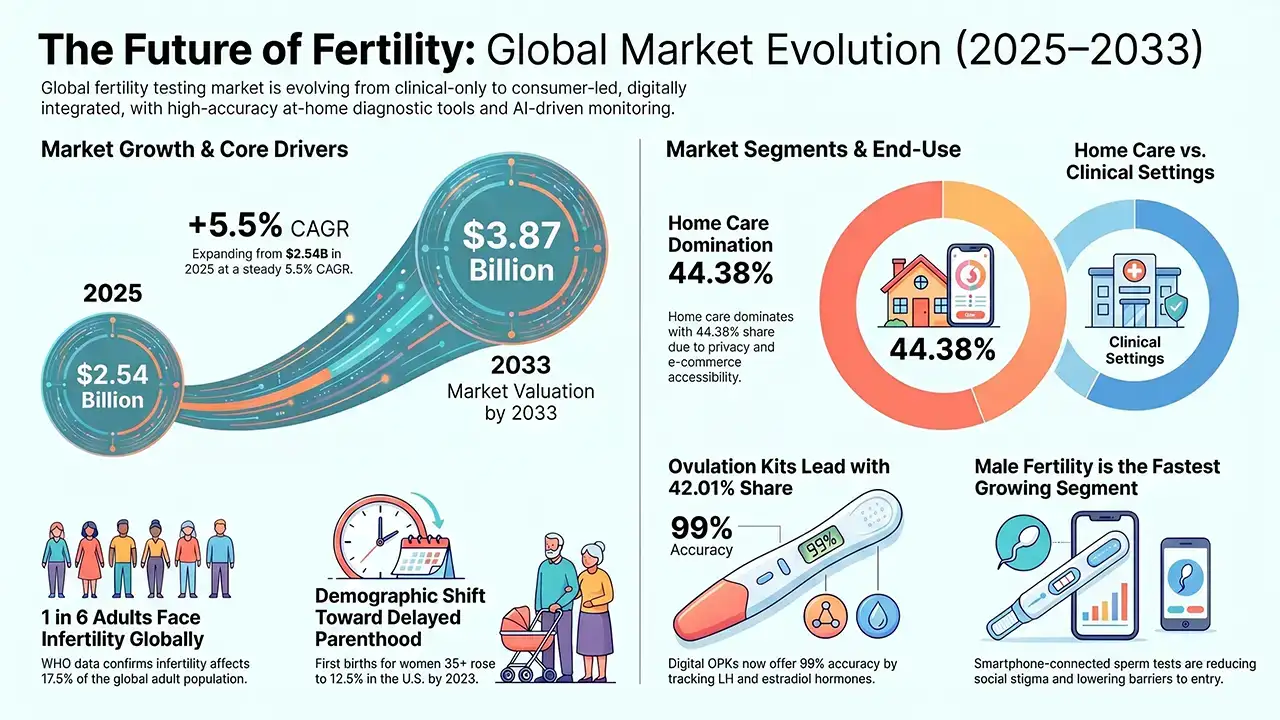

The global Fertility Testing Devices market, valued at USD 2.54 billion in 2025, is projected to reach USD 3.87 billion by 2033, growing at a CAGR of 5.5%. Rising infertility rates, delayed parenthood, and technology-driven at-home testing solutions are fueling robust worldwide demand across North America, Asia Pacific, and beyond.

Researchers at the Babraham Institute and Stanford University have engineered a 3D laboratory model of the human uterus to observe embryo implantation in unprecedented detail, up to day 14 of development. Published in Cell, this breakthrough opens new pathways for understanding IVF failure, miscarriage, and pregnancy complications.

Global fertility tourism is projected to reach US$13,080.0 Mn by 2032 at a 30.3% CAGR, led by IVF and a strong North America share.

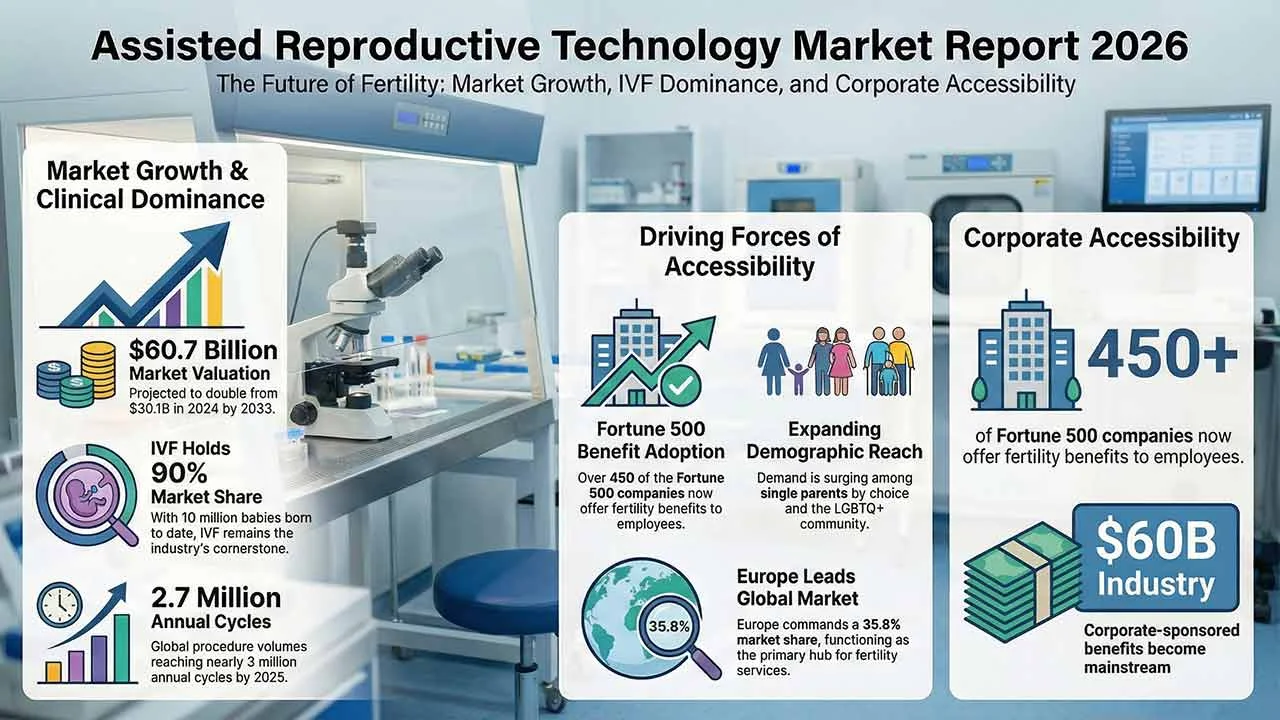

The assisted reproductive technology market continues to expand as infertility rates rise and parenthood is increasingly delayed worldwide. Valued at US$30.1 billion in 2024, the market is projected to reach US$60.7 billion by 2033, supported by IVF innovation, growing awareness, improved accessibility, and sustained investment in reproductive healthcare infrastructure globally.

The global human reproductive technology market is set to reach 45.4 USD billion by 2035, expanding from 27.7 USD billion in 2024 at a 4.6% CAGR. Growth is fueled by technological advancements in fertility treatments, rising infertility rates, delayed pregnancies, and increasing acceptance of single and LGBTQ+ parenting worldwide.

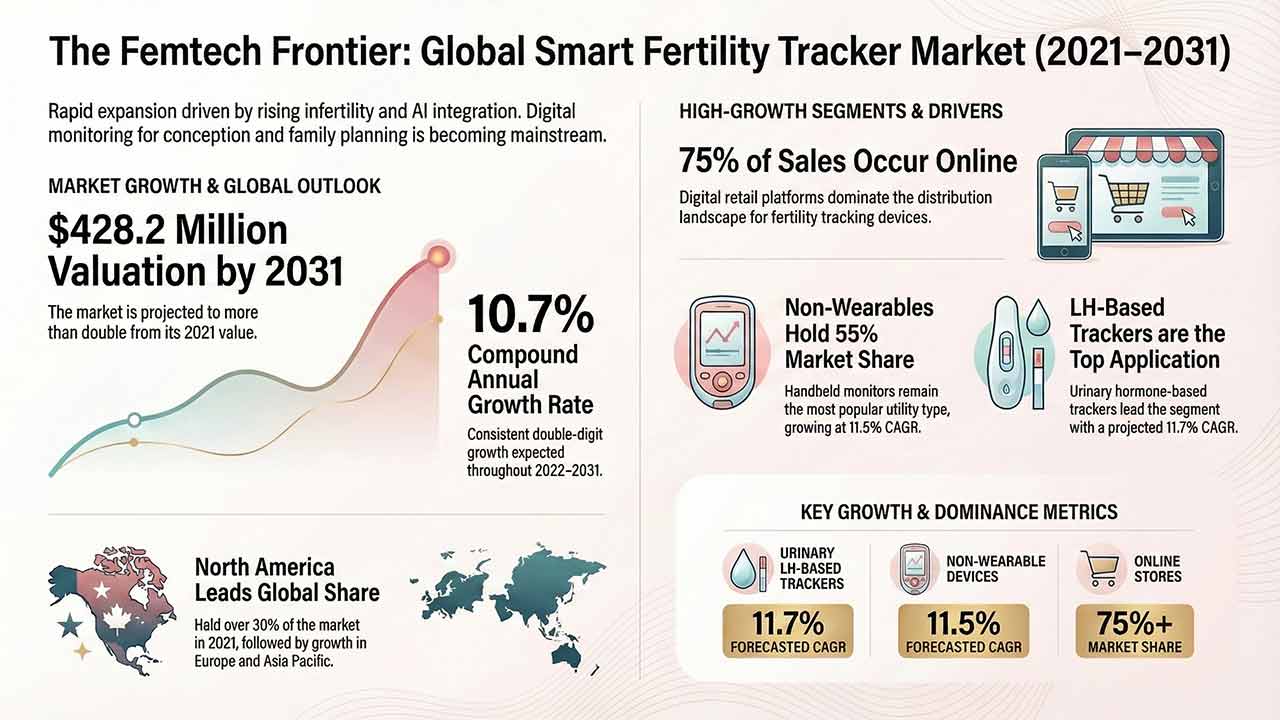

This comprehensive report analyses the Smart Fertility Tracker Market, detailing its projected growth from US$ 160.2 million in 2021 to US$ 428.2 million by 2031. It examines key drivers such as rising infertility and technological advancements in AI-integrated hormone monitoring, alongside detailed segmentation by utility, application, and region.

The Sperm Separation Systems Market is projected to exceed USD 1.5 billion by 2035, driven by automation, microfluidics, and rising male infertility awareness.