Home

ReportReport

ReportReportThe global surrogacy market, valued at USD 204.6 million in 2025, is projected to reach USD 329.2 million by 2034 at a CAGR of 5.43%. Rising infertility rates, expanding LGBTQ+ family-building demand, and advancements in IVF technology are driving sustained growth across North America, Europe, and the Asia Pacific region.

The global landscape of family building is being fundamentally reshaped by a convergence of demographic, medical, and sociocultural forces and at the centre of this transformation sits the global surrogacy market. Once a niche arrangement practised quietly in a handful of jurisdictions, surrogacy has evolved into a globally recognised, medically sophisticated, and increasingly regulated pathway to parenthood. Today, it serves an expanding cohort of intended parents that includes heterosexual couples facing medical infertility, same-sex and LGBTQ+ individuals building families, and single individuals pursuing parenthood outside traditional partnerships.

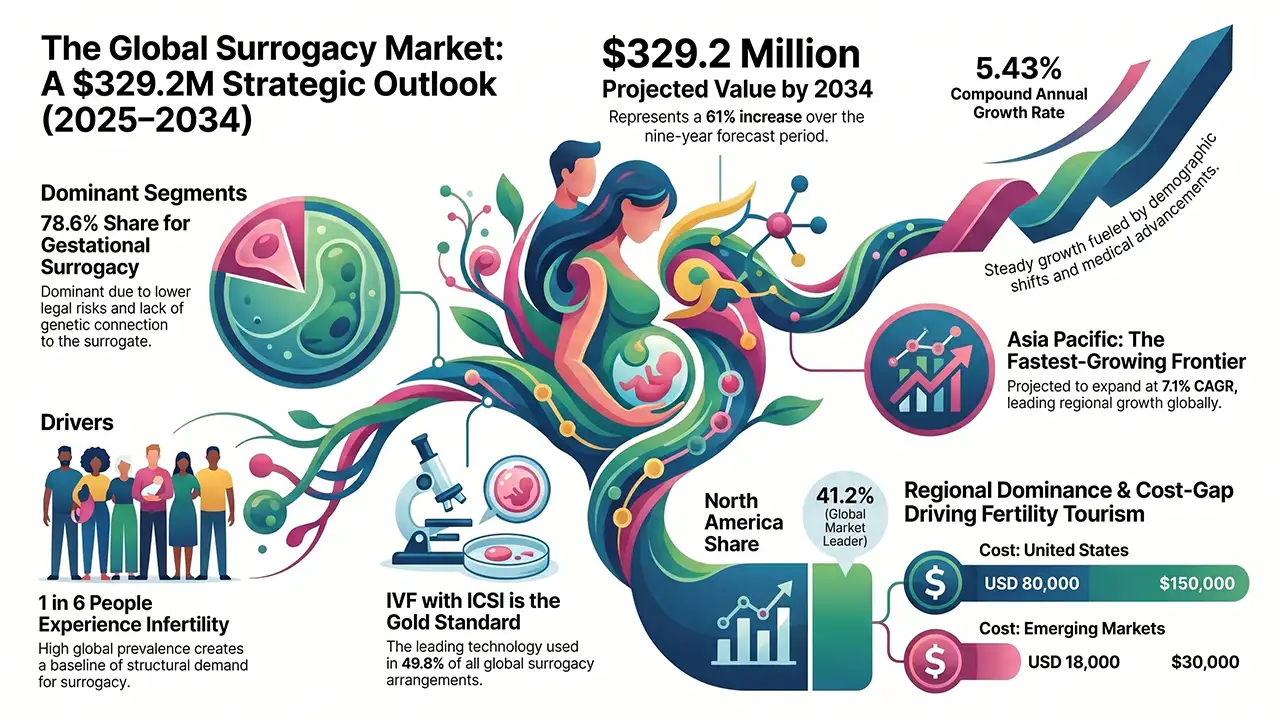

Valued at USD 204.6 million in 2025, the global surrogacy market is projected to reach USD 329.2 million by 2034, advancing at a compound annual growth rate (CAGR) of 5.43% during the period 2026 to 2034, according to IMARC Group. This trajectory reflects not merely a growing commercial sector but a broader social evolution, one in which advances in assisted reproductive technology (ART), evolving legal frameworks, and expanding awareness of reproductive options are collectively increasing access to surrogacy for intended parents across income levels and geographies.

The global surrogacy market entered 2025 with a confirmed value of USD 204.6 million, representing the cumulative result of steady historical growth since 2020. The forecast horizon 2026 to 2034 is expected to deliver consistent and meaningful expansion at a 5.43% CAGR, producing a market valued at approximately USD 329.2 million by 2034 a gain of roughly 61% over nine years. This is a market defined not by speculative growth but by structural inevitability: the forces driving demand are rooted in biology, demography, and enduring social change.

Three structural forces are sustaining this trajectory. First, the rising global prevalence of infertility and delayed parenthood in high-income economies. Second, the increasing legal recognition and societal normalisation of gestational surrogacy across key markets. Third, the growing availability of affordable surrogacy destinations through expanding fertility tourism corridors that allow intended parents in restrictive jurisdictions to access services in permissive ones. These forces are mutually reinforcing: as legal frameworks mature, medical confidence improves; as clinical outcomes improve, more intended parents choose surrogacy; and as demand grows, more jurisdictions invest in supportive legal infrastructure.

Three structural forces are sustaining this trajectory. First, the rising global prevalence of infertility and delayed parenthood in high-income economies. Second, the increasing legal recognition and societal normalisation of gestational surrogacy across key markets. Third, the growing availability of affordable surrogacy destinations through expanding fertility tourism corridors that allow intended parents in restrictive jurisdictions to access services in permissive ones. These forces are mutually reinforcing: as legal frameworks mature, medical confidence improves; as clinical outcomes improve, more intended parents choose surrogacy; and as demand grows, more jurisdictions invest in supportive legal infrastructure.

Several powerful and interconnected forces underpin the upward trajectory of the global surrogacy market through 2034. Each driver reinforces the others, creating a durable and compounding cycle of awareness, demand, and innovation.

Rising global infertility rates are the primary structural driver of surrogacy demand. The World Health Organization (WHO) estimates that approximately 17.5% of the adult global population, roughly 1 in 6 individuals, experience infertility at some point in their lives, creating persistent demand for advanced reproductive pathways. Surrogacy is increasingly positioned as the definitive solution for women with uterine conditions such as Mayer-Rokitansky-Küster-Hauser (MRKH) syndrome, Asherman syndrome or those who have undergone hysterectomy, as well as those experiencing recurrent pregnancy loss. The scale of this unmet medical need anchors the global surrogacy market's baseline demand and ensures that even modest improvements in market access translate into meaningful growth.

Technological advances in ART are raising clinical confidence in surrogacy outcomes and expanding the range of intended parent profiles for whom the pathway is viable. Preimplantation Genetic Testing, specifically PGT-A (aneuploidy screening) and PGT-M (monogenic disease testing), has reduced miscarriage rates by half in gestational surrogacy cycles by enabling the selection of chromosomally normal embryos before transfer. Combined with blastocyst culture, time-lapse embryo monitoring, and improved cryopreservation protocols, these advances are making surrogacy cycles more predictable and commercially viable for clinics and intended parents alike. ICSI achieves fertilization rates of 70–80% per mature egg through direct sperm injection — a critical performance advantage in surrogacy arrangements where embryo quality and transfer reliability are paramount.

The normalisation of LGBTQ+ family-building represents a structurally new and rapidly expanding demand cohort. With 39 countries having legalised same-sex marriage and with corporate America steadily expanding fertility benefit coverage to include same-sex couples, LGBTQ+ individuals, particularly male same-sex couples and single fathers-by-choice, are becoming an increasingly significant share of intended parents in gestational surrogacy arrangements. A 2025 Society for Human Resource Management (SHRM) Employee Benefits Survey found that 24% of employers provide coverage for IVF procedures, with surrogacy coverage representing the highest-value tier of fertility benefits as more progressive employers integrate full family-building support into compensation packages. Global fertility technology investment exceeded USD 1.5 billion in 2024, further broadening the infrastructure supporting surrogacy services.

The cost differential between surrogacy destinations is a powerful structural driver of fertility tourism as a market channel. Commercial gestational surrogacy in the United States ranges from USD 80,000 to USD 150,000, while comparable clinical services are available for USD 18,000 to USD 30,000 in alternative jurisdictions with adequate legal frameworks. This stark differential creates a structural incentive for cost-sensitive intended parents to access international surrogacy services, spawning a sophisticated cross-border ecosystem of agencies, legal specialists, and clinical coordinators that constitutes one of the market's fastest-growing operating segments.

North America commanded 41.2% of the global surrogacy market in 2025 — the world's largest and most commercially developed surrogacy ecosystem. The United States anchors this regional leadership through comprehensive state-level legal frameworks: California, Nevada, and Washington provide enforceable pre-birth orders and gestational carrier agreements that protect all parties and establish parentage with clarity before birth. This legal infrastructure has cultivated a mature ecosystem of fertility clinics, dedicated surrogacy agencies, reproductive law firms, and mental health counsellors with standardized operational protocols. Expanding employer fertility benefit coverage, with 24% of US employers now providing IVF coverage per the 2025 SHRM survey, is progressively lowering the financial barrier for middle-income intended parents and broadening the addressable market beyond the high-net-worth cohort.

Europe, at 24.8% market share, represents a highly diverse regulatory environment. Greece, as the first European country to legalise altruistic surrogacy for foreign nationals, has emerged as the preferred destination for European intended parents unable to pursue surrogacy domestically. Ukraine, historically the continent's leading commercial surrogacy destination, has seen market disruption from geopolitical developments, accelerating the diversification of intended parent flows toward Georgia and Portugal. UK Law Commission reform discussions, potentially opening regulated domestic altruistic surrogacy, represent a significant latent opportunity; domestic legalisation in the UK alone could meaningfully expand European market capacity.

The Asia Pacific, currently holding a 22.6% market share, is the highest-growth regional opportunity, projected to expand at approximately a 7.1% CAGR through 2034, the fastest regional growth rate in the global surrogacy market. Expanding fertility tourism into Georgia and select emerging markets, domestic IVF growth in India and Australia, and rising infertility awareness in Japan, South Korea, and China are the primary drivers. India's Surrogacy (Regulation) Act, 2021, which banned commercial surrogacy for foreign nationals, has redirected international demand to alternative regional destinations, even as domestic altruistic surrogacy and IVF services in India represent a high-growth segment (Nova IVF opened its 100th Indian fertility centre in Jammu in July 2025). The most significant regional development in the near term is Thailand's March 2026 preparations to reopen its international surrogacy market after a near decade-long ban, with proposed regulations allowing legally married foreign couples, including same-sex couples, to pursue surrogacy under stricter government oversight.

Latin America, at 6.4%, is emerging as a meaningful growth market, with Mexico and Colombia positioned as affordable and legally navigable cross-border surrogacy alternatives to the US for cost-sensitive intended parents from the Americas. Cultural stigmas around fertility are gradually diminishing as urban middle-class awareness rises. The Middle East & Africa (5.0%) is anchored by UAE and Israel as developing regional fertility hubs, IVIRMA Global's July 2025 acquisition of ART Fertility Clinics' operations in the UAE and Saudi Arabia directly reflects rising demand from Gulf Cooperation Council nationals. Israel's landmark 2021 ruling expanding LGBTQ+ access to surrogacy domestically represents a notable policy shift in the region.

Despite robust demand fundamentals, the global surrogacy market faces meaningful structural restraints. Legal restrictions and regulatory uncertainty represent the most significant barrier to market expansion. Surrogacy remains legally prohibited or wholly unregulated in Germany, France, Italy, Spain, China, and much of the Middle East. India's 2022 ban on commercial surrogacy for foreign nationals significantly restricted a previously major cross-border destination. Varying legal frameworks across jurisdictions create complex compliance environments for international agencies and intended parents navigating multi-country arrangements — and in rare cases, create stateless children as an unintended consequence of surrogacy arrangements in countries with jus sanguinis citizenship laws.

High costs and limited insurance coverage further constrain market accessibility. Commercial gestational surrogacy in the United States costs USD 80,000–150,000 for intended parents, encompassing agency fees, surrogate compensation, legal fees, and IVF cycles. Currently, only 25 US states and Washington D.C. mandate private insurance coverage for fertility care, and surrogacy-specific coverage remains limited – creating significant financial barriers for middle-income intended parents and suppressing potential demand that would otherwise materialise. Surrogate supply constraints add a further structural limitation: approximately 20,000–30,000 surrogate births take place annually worldwide, with 4–12 months of matching time required and stringent medical, psychological, and lifestyle screening criteria limiting the qualified surrogate pool.

The global surrogacy market stands at a pivotal moment in its evolution. Growing from USD 204.6 million in 2025 to a projected USD 329.2 million by 2034, the market is expanding on the back of some of the most powerful and enduring trends in modern healthcare: the global infertility epidemic, the normalisation of LGBTQ+ family-building, the democratisation of ART through employer benefit coverage, and the technological maturation of IVF and embryo selection. For intended parents, the path to parenthood through surrogacy is becoming more accessible, more clinically reliable, and more legally protected than at any prior point in history.

For investors and industry participants, the global surrogacy market represents a compelling convergence of demographic necessity, technological innovation, and expanding institutional support. The fastest-growing vectors, IVF with ICSI technology (~6.2% CAGR), gestational surrogacy type (~5.8% CAGR), and the Asia Pacific region (~7.1% CAGR), define the strategic priorities for the 2026–2034 period. Employer fertility benefit integration, AI-enabled embryo selection, and cross-border surrogacy service infrastructure represent the investment and partnership themes most likely to drive outperformance within the forecast window. The global surrogacy market is a space where structural demand consistently outpaces the legal frameworks designed to govern it, ensuring that the gap between global fertility need and accessible surrogacy capacity will continue to drive growth well beyond the 2034 forecast horizon.

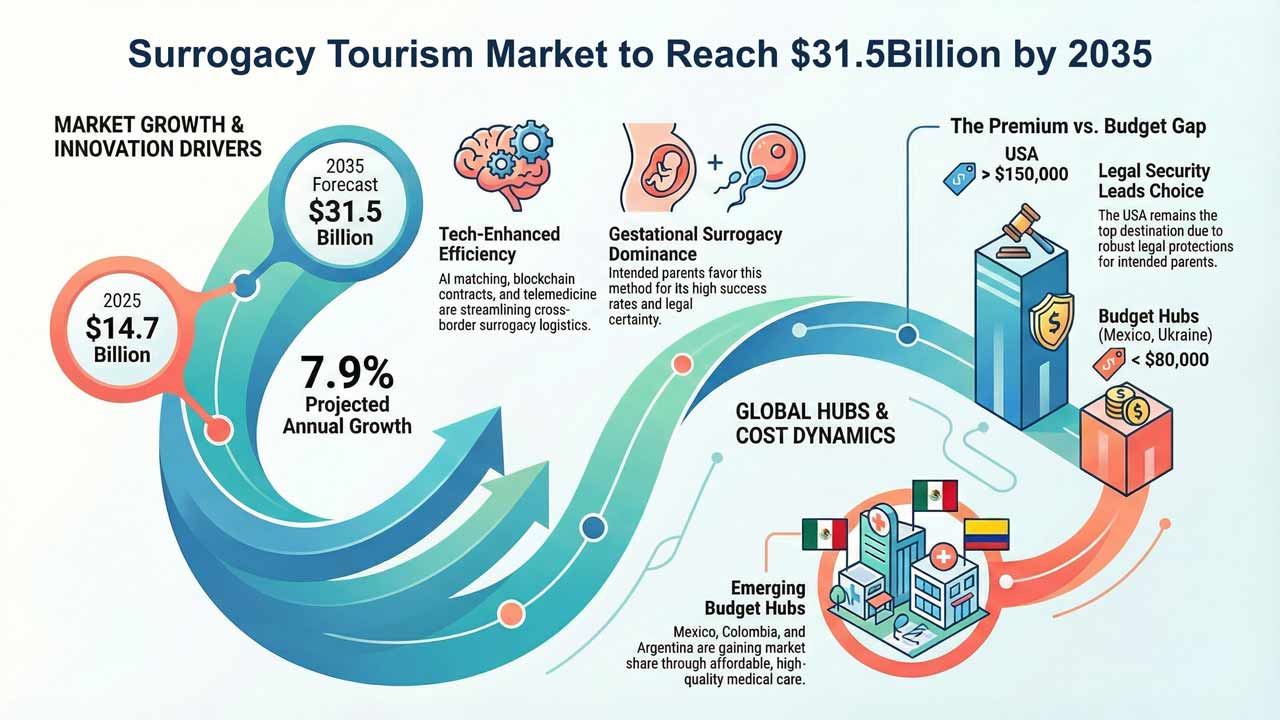

The surrogacy tourism market is projected to reach USD 31.5 billion by 2035, fueled by rising infertility, evolving legal frameworks, and technological integration. Cross-border demand, AI-powered matching, blockchain contracts, and expanding access in Latin America and Eastern Europe are reshaping global family-building pathways.