Home

ReportReport

ReportReportThe Sperm Separation Systems Market is projected to exceed USD 1.5 billion by 2035, driven by automation, microfluidics, and rising male infertility awareness.

The Sperm Separation Systems Market is entering a pivotal growth phase in assisted reproductive technologies, underpinned by clinical adoption across IVF centers, fertility hospitals, and labs seeking higher efficiency and standardized outcomes. In 2024, the market achieved USD 468.3 million, reflecting robust demand for next-generation sperm isolation tools optimized for quality, safety, and reproducibility. By 2035, the market is expected to exceed USD 1.5 billion, signaling a mature transformation aided by automation, digitization, and patient-centric fertility care models. This trajectory is reinforced by rising awareness of male infertility and the shift toward precise, non-invasive selection methods. The Sperm Separation Systems Market is thus strategically positioned at the intersection of clinical performance and scalable, tech-forward fertility workflows.

Global momentum is evident as advanced separation systems migrate from traditional density gradient and swim-up methods to microfluidics, electrophoresis, and MACS/LACS technologies that better emulate physiological pathways. The market stood at USD 468.3 million in 2024 and is projected to surpass USD 1.5 billion by 2035, reflecting enduring capital investments into semi- and fully automated lab platforms and integrated software for traceability and compliance. North America leads adoption, followed by Europe and Asia Pacific, with demand supported by improved access and infrastructure in key fertility hubs. Collectively, these dynamics point toward a market defined by higher throughput, lower manual variability, and quantifiable gains in ART laboratory consistency. The Sperm Separation Systems Market is expected to benefit from institutional networks prioritizing digitized, reproducible, and quality-assured sperm selection.

Technological shifts are reshaping the standard of care as microfluidic cartridge systems enable gentler, non-centrifugation workflows that preserve DNA integrity and motility profiles integral to ART outcomes. Parallelly, AI-enabled analytics and real-time monitoring are expanding quality oversight, ensuring sample traceability and alignment with accreditation standards across diverse clinical environments. Leaders are bundling devices with software and training under subscription-based ecosystems to enhance stickiness and lifetime value. Additionally, cross-sector partnerships between fertility tech providers, hospital networks, and academia are accelerating validation cycles and expanding clinical readiness for next-gen sperm selection modules in the Sperm

Separation Systems Market.

Despite strong growth signals, high upfront costs for automated systems may constrain adoption among smaller and mid-sized clinics, creating a capex barrier that necessitates creative financing or service-led models. Workforce constraints persist in several developing regions, where a shortage of skilled professionals can limit the practical implementation of advanced platforms without sustained training programs. Ethical and regulatory variability across jurisdictions introduces complexity for market entry, certification, and longitudinal data practices. Finally, stringent, multi-country approval pathways can extend time-to-market and require significant clinical and regulatory investment for vendors in the Sperm Separation Systems Market.

Expansion of fertility infrastructure in emerging markets such as India, Brazil, and China presents attractive growth runways for manufacturers and integrated platform providers. Demand is expected to rise for automated, portable systems that scale effectively within medium-sized clinics, enhancing access while maintaining consistency and throughput. Precision-based reproductive care, including genetic screening alignment, is catalyzing interest in high-fidelity selection tools that reduce fragmentation risk and elevate clinical outcomes. The integration of AI, robotics, and microfluidics under unified workflows positions the Sperm Separation Systems Market to deliver standardized, data-rich selection pathways with measurable clinical KPIs.

North America: The region leads global share due to advanced healthcare infrastructure, employer fertility benefits, and strong ART utilization, creating favorable conditions for automated, AI-integrated platforms and software-driven quality control. Concentrated IVF networks and central labs further support scale and consistency in deployment.

Competition is characterized by product portfolio expansion, IP consolidation, and digital analytics integration among established and emerging players. Notable companies include CooperSurgical, Vitrolife, Hamilton Thorne, Memphasys, NidaCon, FertiPro, FUJIFILM Irvine Scientific, Merck, Miltenyi Biotec, SperogenX Biosciences, and Promega, each leveraging R&D collaboration for clinical adoption. Recent actions include CooperSurgical’s acquisition of ZyMōt Fertility in June 2024 to integrate patented motile-sperm selection and Memphasys’ 2023 expansion in Asia with the Felix system’s entry into Japan after traction in India, New Zealand, and Canada. Software modules launched in 2024 enhanced real-time tracking and performance metrics for transparent, standards-aligned workflows in the Sperm Separation Systems Market.

Vendors align offerings across product type (semen separation kits, processing equipment, freezing equipment, chemicals), technology (density gradient, modified swim-up, microfluidics, MACS, LACS), and operation modes (manual, semi-automated, fully automated). Applications span IVF, ICSI, artificial insemination, sperm banking, and related use cases, serving hospitals and clinics, cryobanks, fertility centers/IVF labs, and research institutions across major global regions. Clear segmentation supports tailored commercialization and compliance strategies in the Sperm Separation Systems Market.

With the market projected to rise from USD 468.3 million in 2024 to over USD 1.5 billion by 2035, the Sperm Separation Systems Market is set to be defined by automation, AI-anchored quality systems, and microfluidics that reduce variability and preserve sperm integrity. Regional leadership in North America and strong advances in Europe and Asia Pacific will anchor global demand, while opportunities in emerging economies broaden the addressable base. As clinical networks prioritize standardization and outcomes, integrated device-software ecosystems and collaborative R&D will shape the next era of precision fertility technology and scalable ART excellence.

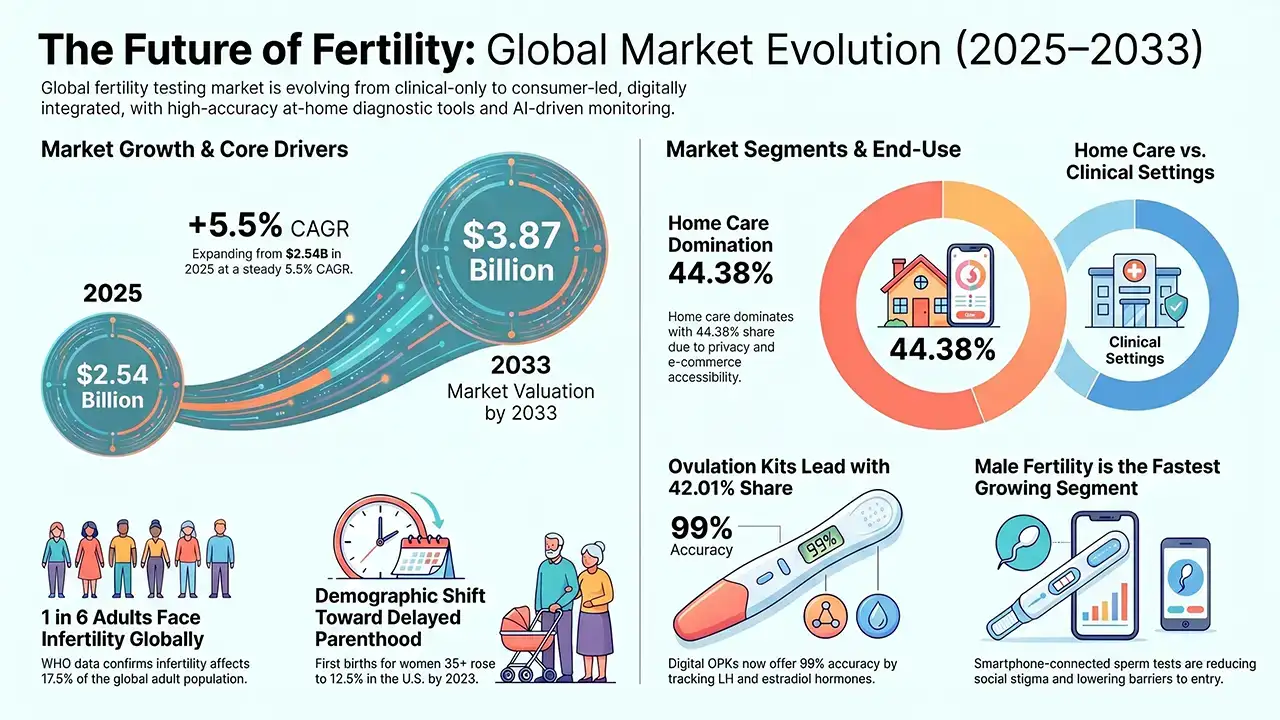

The global Fertility Testing Devices market, valued at USD 2.54 billion in 2025, is projected to reach USD 3.87 billion by 2033, growing at a CAGR of 5.5%. Rising infertility rates, delayed parenthood, and technology-driven at-home testing solutions are fueling robust worldwide demand across North America, Asia Pacific, and beyond.

Researchers at the Babraham Institute and Stanford University have engineered a 3D laboratory model of the human uterus to observe embryo implantation in unprecedented detail, up to day 14 of development. Published in Cell, this breakthrough opens new pathways for understanding IVF failure, miscarriage, and pregnancy complications.

Global fertility tourism is projected to reach US$13,080.0 Mn by 2032 at a 30.3% CAGR, led by IVF and a strong North America share.

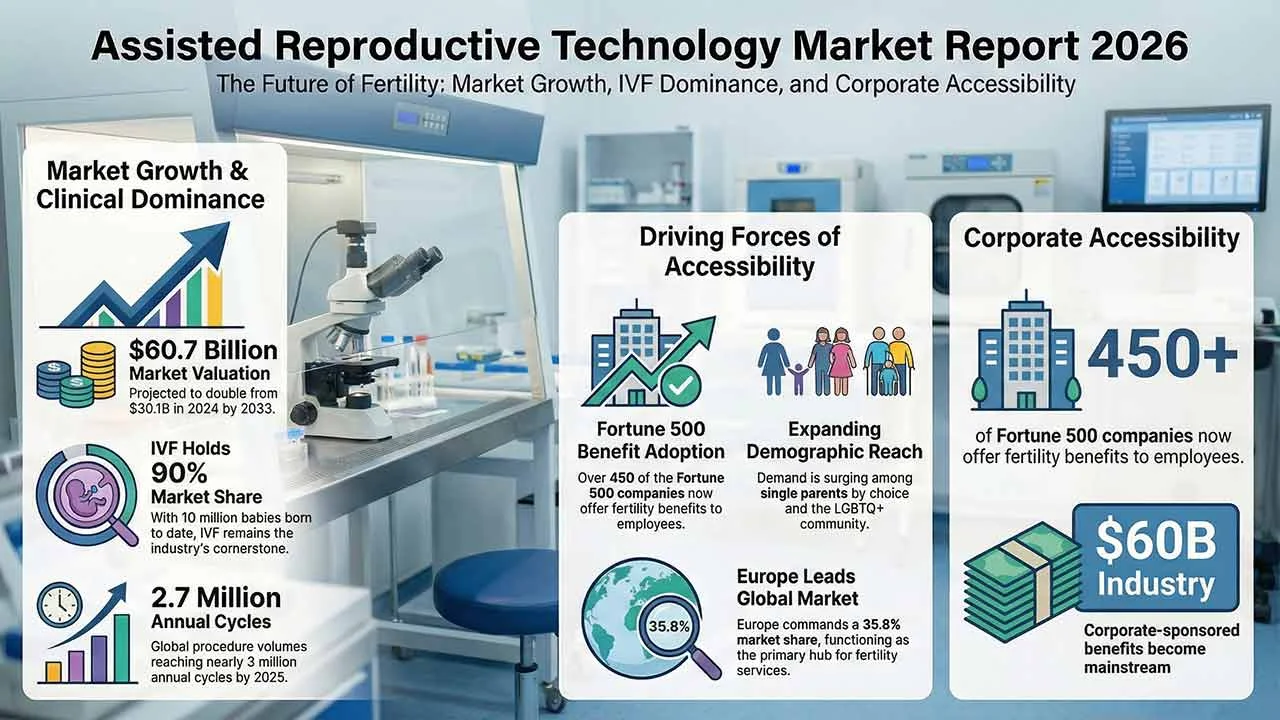

The assisted reproductive technology market continues to expand as infertility rates rise and parenthood is increasingly delayed worldwide. Valued at US$30.1 billion in 2024, the market is projected to reach US$60.7 billion by 2033, supported by IVF innovation, growing awareness, improved accessibility, and sustained investment in reproductive healthcare infrastructure globally.

The global human reproductive technology market is set to reach 45.4 USD billion by 2035, expanding from 27.7 USD billion in 2024 at a 4.6% CAGR. Growth is fueled by technological advancements in fertility treatments, rising infertility rates, delayed pregnancies, and increasing acceptance of single and LGBTQ+ parenting worldwide.

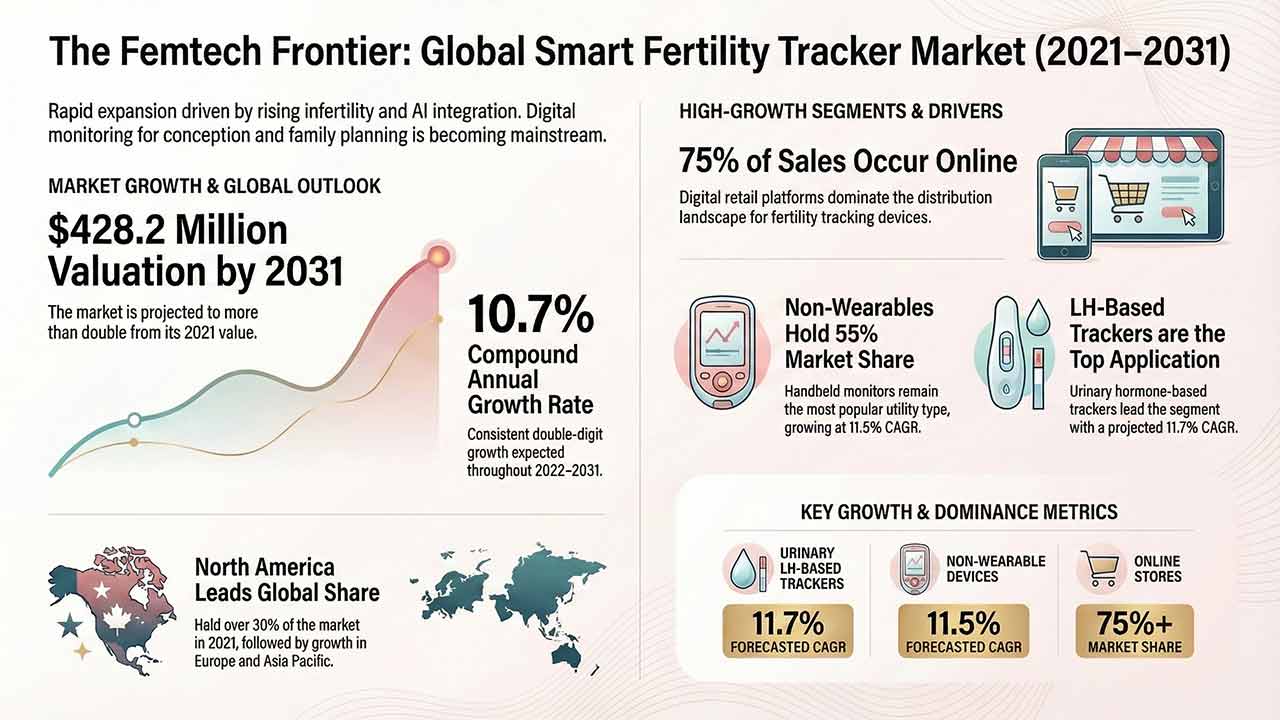

This comprehensive report analyses the Smart Fertility Tracker Market, detailing its projected growth from US$ 160.2 million in 2021 to US$ 428.2 million by 2031. It examines key drivers such as rising infertility and technological advancements in AI-integrated hormone monitoring, alongside detailed segmentation by utility, application, and region.