Home

ReportReport

ReportReportAn analysis of the global infertility treatment devices and equipment industry through 2035. It examines critical market drivers such as delayed childbearing, technological innovations in AI and automation, and regional growth patterns, offering strategic insights into the evolving landscape of assisted reproductive technology worldwide.

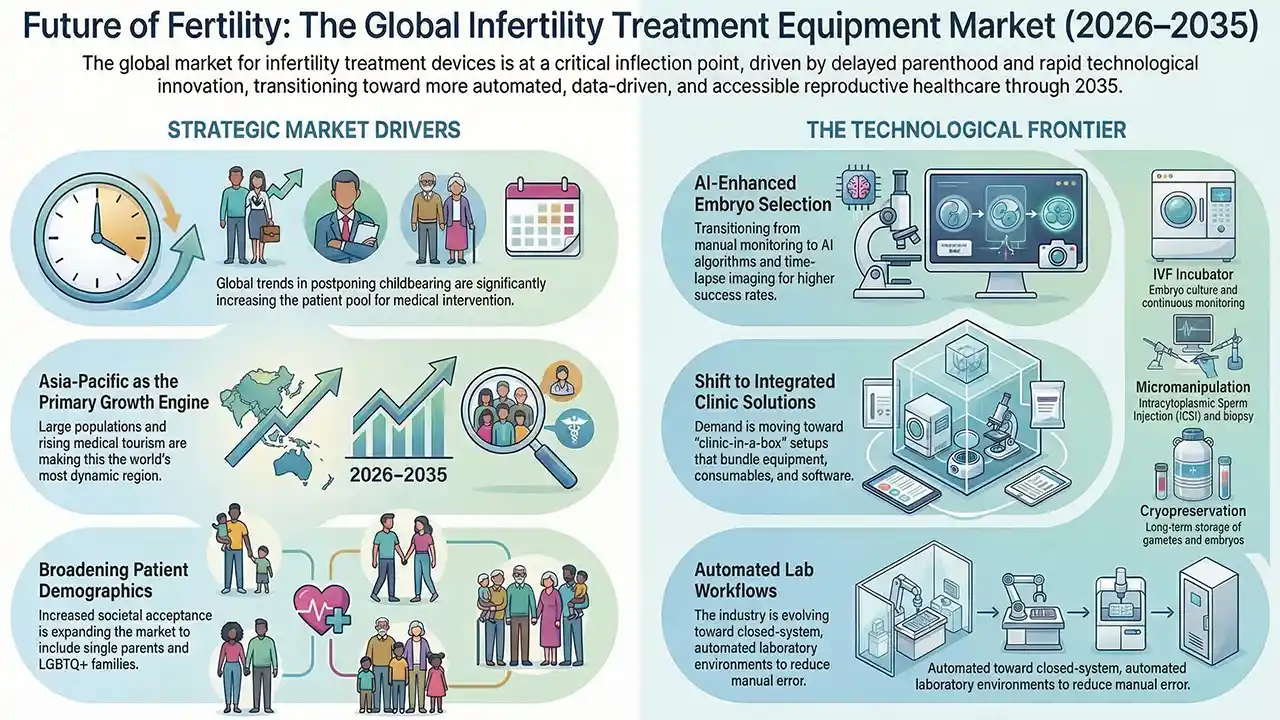

The global market for infertility treatment devices and equipment is currently at a critical inflection point, undergoing a transition from a niche medical sector to a mainstream component of the broader reproductive healthcare landscape. This evolution is underpinned by profound demographic shifts, accelerating technological innovation, and a steady increase in healthcare accessibility across the globe. Driven by rising societal acceptance and urgent demographic needs, the industry is poised for sustained expansion through 2035.

The sector encompasses a specialised array of medical technologies essential for assisted reproductive technology (ART) procedures. The scope includes both capital equipment and single-use consumables utilised in clinical and laboratory settings.

Key product segments covered in the market analysis include:

Growth in the industry is fundamentally underpinned by the rising global prevalence of infertility. Several macro-drivers are expanding the patient pool and, consequently, the demand for infertility treatment devices and equipment.

The most powerful macro-driver identified is the widespread trend of delayed childbearing, particularly in urbanised and developed economies. As individuals and couples postpone starting families for career, educational, or financial reasons, the age-related decline in fertility naturally increases the need for medical intervention. Furthermore, societal transformations, including reduced stigma, increased public awareness, and evolving family structures (such as support for single parents and LGBTQ+ families), have significantly broadened the addressable market.

Improving insurance coverage and reimbursement policies in key markets are lowering financial barriers for patients. This shift from purely out-of-pocket expenses to partially covered treatments is making advanced ART procedures accessible to a larger socioeconomic demographic. Additionally, the shift from hospital-based treatments to dedicated outpatient fertility clinics has created a distinct demand profile focused on equipment reliability and space efficiency.

Technology is the primary catalyst for market evolution, with the clinical pursuit of higher success rates driving the adoption of advanced apparatus.

Contemporary demand is shaped by the adoption of time-lapse incubators with integrated imaging, which allow for continuous embryo monitoring without environmental disturbance. Advanced laser systems are also increasingly utilised for precise embryo biopsies during preimplantation genetic testing (PGT).

Looking toward 2035, the integration of digital tools and data analytics is expected to become pervasive. Key shifts in the forecast period include:

The global market exhibits a multipolar structure with varying growth trajectories across different geographies.

North America and Western Europe remain high-volume, mature markets. These regions are characterised by well-established regulatory frameworks, high patient expenditure, and a concentration of manufacturing hubs. Germany is identified as a leading exporter of precision laboratory equipment, while the United States remains a major importer and a leader in advanced imaging technologies.

The Asia-Pacific region has emerged as the most dynamic growth engine for the industry. This growth is fuelled by large population bases, improving economic conditions, and growing medical tourism. Countries like Vietnam are showing some of the fastest import growth rates globally. Furthermore, production is increasingly shifting toward China and South Korea, which possess strong biomedical engineering capabilities.

Emerging economies in Latin America, the Middle East, and Africa are witnessing increased market penetration. While growth in these regions is sometimes constrained by economic volatility and infrastructure gaps, they are expected to account for a larger share of incremental demand by 2035 as healthcare affordability increases.

Manufacturing in this sector is knowledge-intensive and requires adherence to stringent quality standards due to the sensitivity of the biological materials involved.

Manufacturing sites are predominantly located in regions with high-tech expertise, including the U.S., Europe, Japan, and increasingly, East Asia. While capital equipment production is highly concentrated, the manufacturing of disposable consumables is more geographically dispersed to optimise costs and meet local regulatory requirements.

Logistics for infertility treatment devices and equipment present unique challenges. Highly sensitive equipment like microscopes and laser systems requires specialised packaging to protect against shock and temperature fluctuations. Furthermore, the transport of controlled-rate cryogenic tanks necessitates expert providers capable of managing liquid nitrogen levels and navigating complex international biosecurity regulations.

Pricing in the market is highly stratified. At the premium end, sophisticated capital equipment, such as integrated time-lapse systems, commands high prices justified by improved clinical outcomes and lab efficiency. In contrast, standard incubators and workstations face more direct price competition.

The consumables segment operates on a recurring revenue model. While some basic items face commoditisation pressure, innovative consumables like next-generation vitrification kits maintain strong pricing power. Additionally, the bargaining power of large, consolidated fertility clinic chains is growing, which may exert downward pressure on manufacturer margins over the next decade.

Despite the positive outlook, the industry faces significant hurdles:

The trajectory for the infertility treatment devices and equipment market through 2035 points toward sustained but uneven growth. The industry will likely be defined by a shift toward more personalised and predictive medicine, supported by AI and automation. Stakeholders will need to balance the dual needs of enhancing clinical success rates while improving the operational economics of clinics. Ultimately, the market's success over the coming decade will be measured not just by financial scale but by its ability to translate technological innovation into increased access and improved outcomes for patients worldwide.

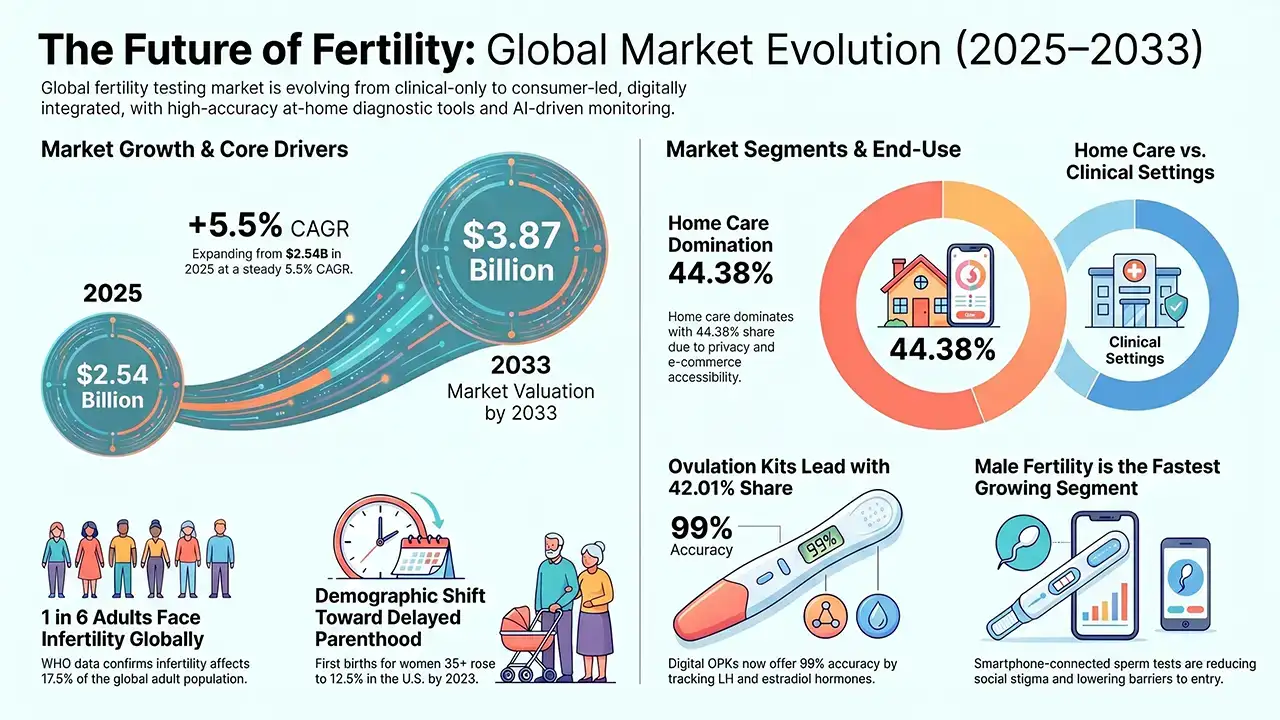

The global Fertility Testing Devices market, valued at USD 2.54 billion in 2025, is projected to reach USD 3.87 billion by 2033, growing at a CAGR of 5.5%. Rising infertility rates, delayed parenthood, and technology-driven at-home testing solutions are fueling robust worldwide demand across North America, Asia Pacific, and beyond.

Researchers at the Babraham Institute and Stanford University have engineered a 3D laboratory model of the human uterus to observe embryo implantation in unprecedented detail, up to day 14 of development. Published in Cell, this breakthrough opens new pathways for understanding IVF failure, miscarriage, and pregnancy complications.

Global fertility tourism is projected to reach US$13,080.0 Mn by 2032 at a 30.3% CAGR, led by IVF and a strong North America share.

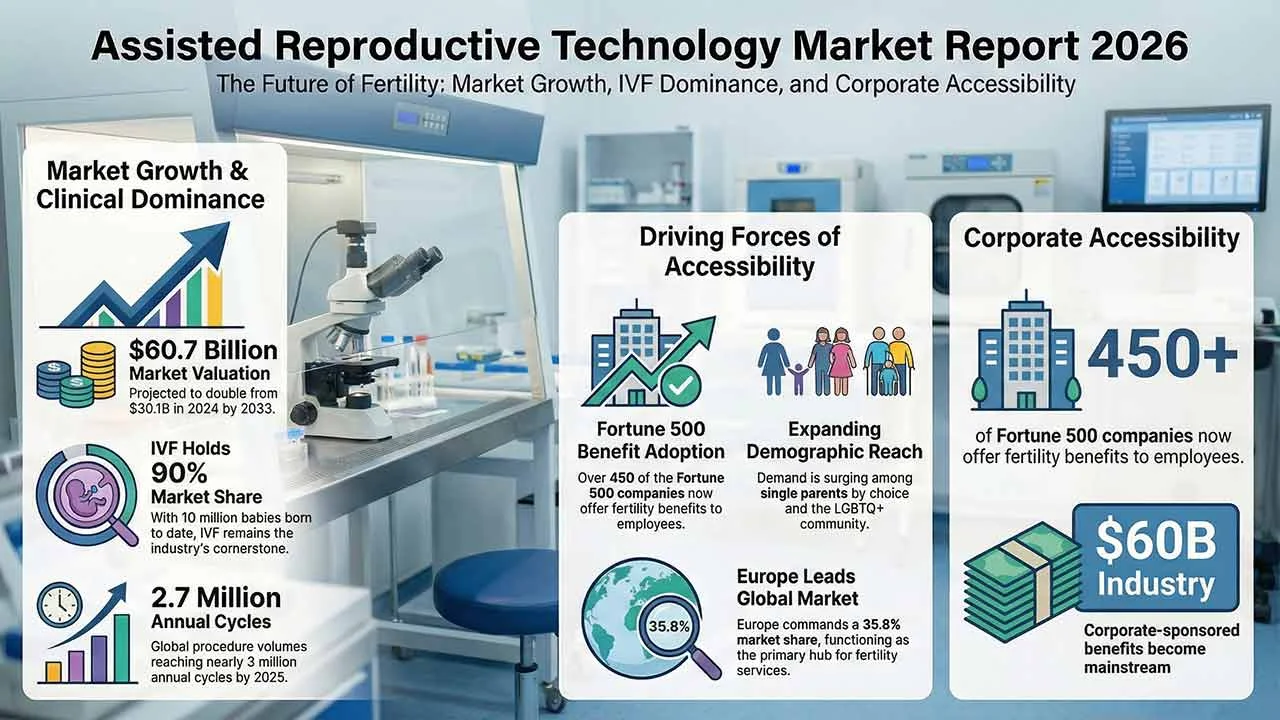

The assisted reproductive technology market continues to expand as infertility rates rise and parenthood is increasingly delayed worldwide. Valued at US$30.1 billion in 2024, the market is projected to reach US$60.7 billion by 2033, supported by IVF innovation, growing awareness, improved accessibility, and sustained investment in reproductive healthcare infrastructure globally.

The global human reproductive technology market is set to reach 45.4 USD billion by 2035, expanding from 27.7 USD billion in 2024 at a 4.6% CAGR. Growth is fueled by technological advancements in fertility treatments, rising infertility rates, delayed pregnancies, and increasing acceptance of single and LGBTQ+ parenting worldwide.

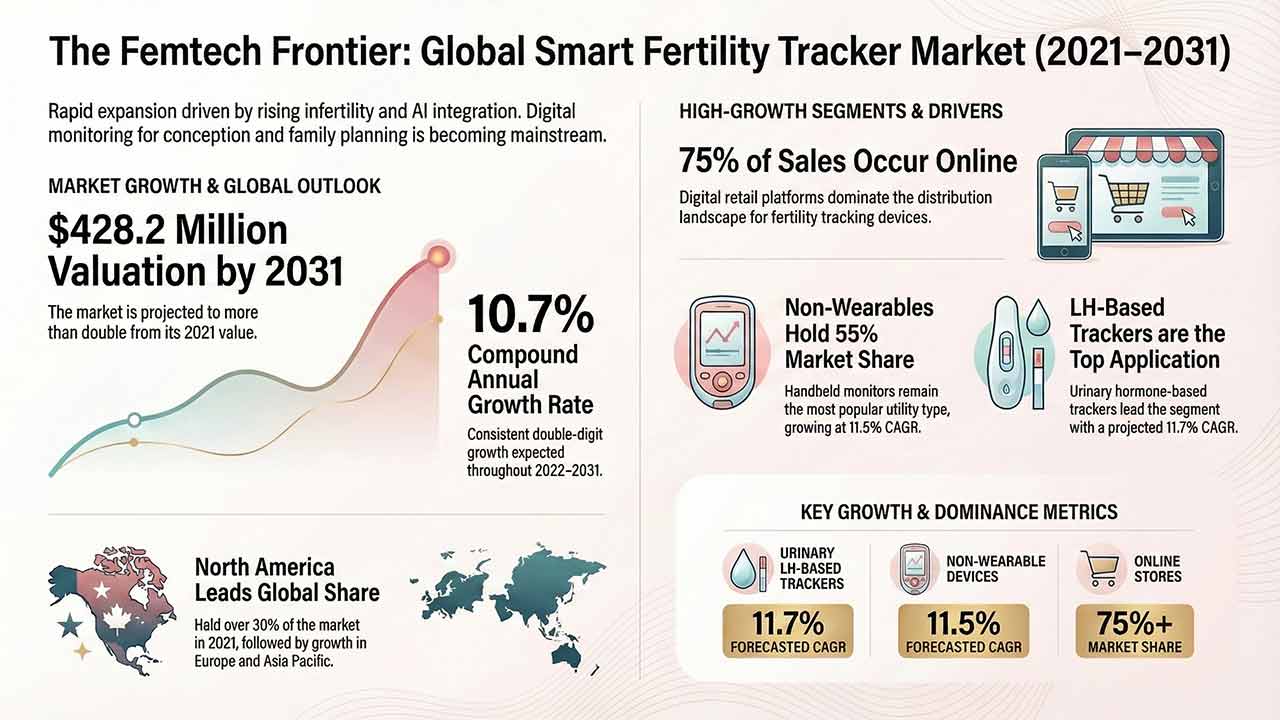

This comprehensive report analyses the Smart Fertility Tracker Market, detailing its projected growth from US$ 160.2 million in 2021 to US$ 428.2 million by 2031. It examines key drivers such as rising infertility and technological advancements in AI-integrated hormone monitoring, alongside detailed segmentation by utility, application, and region.

The Sperm Separation Systems Market is projected to exceed USD 1.5 billion by 2035, driven by automation, microfluidics, and rising male infertility awareness.