Home

ReportReport

ReportReportThe global fertility services market, valued at $35.9 billion in 2024, is projected to reach $80.1 billion by 2033 at a 9.4% CAGR. Growth is fueled by ART advancements, fertility tourism, and rising infertility rates worldwide, positioning the sector as a cornerstone of modern reproductive healthcare.

The global fertility services market demonstrates robust growth potential, valued at $35.9 billion in 2024 and projected to reach $ 80.1 billion by 2033, representing a compound annual growth rate (CAGR) of 9.4% during the forecast period. This significant expansion reflects the increasing global demand for assisted reproductive technologies and comprehensive fertility solutions.

The fertility services market's growth trajectory showcases consistent expansion across the forecast period. The market is expected to experience steady year-over-year growth, driven by technological advancements, increasing awareness, and expanding accessibility to fertility treatments worldwide.

Infertility affects a substantial portion of the global population, with 17.5% of adults experiencing fertility challenges during their lifetime, translating to approximately 1 in 6 people worldwide. The prevalence shows minimal variation across economic regions, with high-income countries reporting 17.8% and low- and middle-income nations at 16.5%. Male factors contribute to approximately 50% of all infertility cases, either as the sole cause or in combination with female factors.

Assisted Reproductive Technology (ART) dominates the fertility services market with a commanding 72% market share, reflecting its critical role in addressing complex fertility challenges. The ART segment's leadership position is supported by continuous technological innovations and proven clinical outcomes.

Fertility clinics represent the largest end-user segment with 67% market share, serving as the primary delivery points for specialized fertility services. These clinics benefit significantly from consolidation, with acquired facilities experiencing a 27% increase in treatment cycles and a 14% improvement in live birth rates.

North America maintains its position as a powerhouse of innovation in the fertility services market. The United States leads with comprehensive infrastructure, including over 450 SART-affiliated clinics and substantial procedure volumes:

Corporate investment continues to fuel market expansion, with Progyny serving over 460 large employer clients as of Q1 2024, and AI fertility startup Alife Health securing over $20 million in funding. The cost structure reflects the premium nature of services, with single IVF cycles reaching $25,000 in major markets like New York City.

Europe maintains unrivaled leadership in advanced reproductive medicine, supported by progressive regulations and high clinical standards. Key European markets demonstrate substantial infrastructure:

The region's advanced infrastructure includes Cryos International shipping to over 100 countries and ESHRE receiving over 2,500 scientific abstracts for its 2024 annual meeting.

The Asia Pacific region represents a region of rapid growth with evolving access and increasing medical tourism. Key developments include:

The fertility services market operates with substantial cost structures reflecting the sophisticated technology and expertise required. Treatment costs vary significantly based on complexity and geographic location:

Laboratory fees can reach $6,000, while specialized PGT services cost up to $5,000 per cycle. Advanced diagnostic equipment, such as high-resolution ultrasound systems designed for fertility applications, carries list prices exceeding $90,000.

Oncofertility represents a critical market driver addressing reproductive preservation for cancer patients. The Oncofertility Consortium recognizes over 150 global partner institutions as of 2024, with significant research investment, including NIH grants exceeding $450,000 for novel preservation methods. Ferring Pharmaceuticals' Heartbeat Program provides up to $10,000 in medications for eligible patients, while leading pediatric hospitals document over 300 fertility preservation consultations annually.

The shift toward non-invasive diagnostics transforms patient experience and clinical outcomes. Major developments include studies of over 2,000 embryos using non-invasive preimplantation genetic testing, $5 million seed funding for microbiome diagnostic platforms, and saliva-based hormone tracking devices priced at $149 enabling daily monitoring without blood draws.

Advanced imaging capabilities now include AI-powered follicle counting tools validated on datasets of over 50,000 ultrasound images, while microfluidics-based sperm sorting reduces processing time to under 30 minutes.

Global fertility clinic infrastructure varies significantly across regions, reflecting different healthcare systems and regulatory environments:

Clinical consolidation demonstrates clear performance benefits, with acquired clinics showing measurable improvements in key operational metrics:

The fertility services market trajectory through 2033 indicates sustained growth driven by multiple converging factors: demographic trends toward delayed childbearing, increasing male fertility challenges, technological innovations in ART procedures, expanding insurance coverage, and growing acceptance of fertility preservation.

Cross-border fertility tourism continues expanding, with approximately 25,000 fertility tourists annually seeking treatment in the United States alone. The research pipeline remains robust, with over 300 active IVF-related clinical trials registered in the U.S. as of mid-2024, promising continued technological advancement.

The market's evolution toward over 93% single embryo transfers in U.S. cycles demonstrates the industry's commitment to safer, more effective protocols while maintaining high success rates. This trend, combined with over 10 million infants born worldwide from IVF cumulatively, establishes ART as a mainstream medical solution for fertility challenges.

Storage and preservation services represent significant long-term growth opportunities, with 111,288 patients maintaining embryos in storage in the UK alone, representing a substantial asset base for clinical providers and ongoing revenue streams supporting market sustainability through 2033.

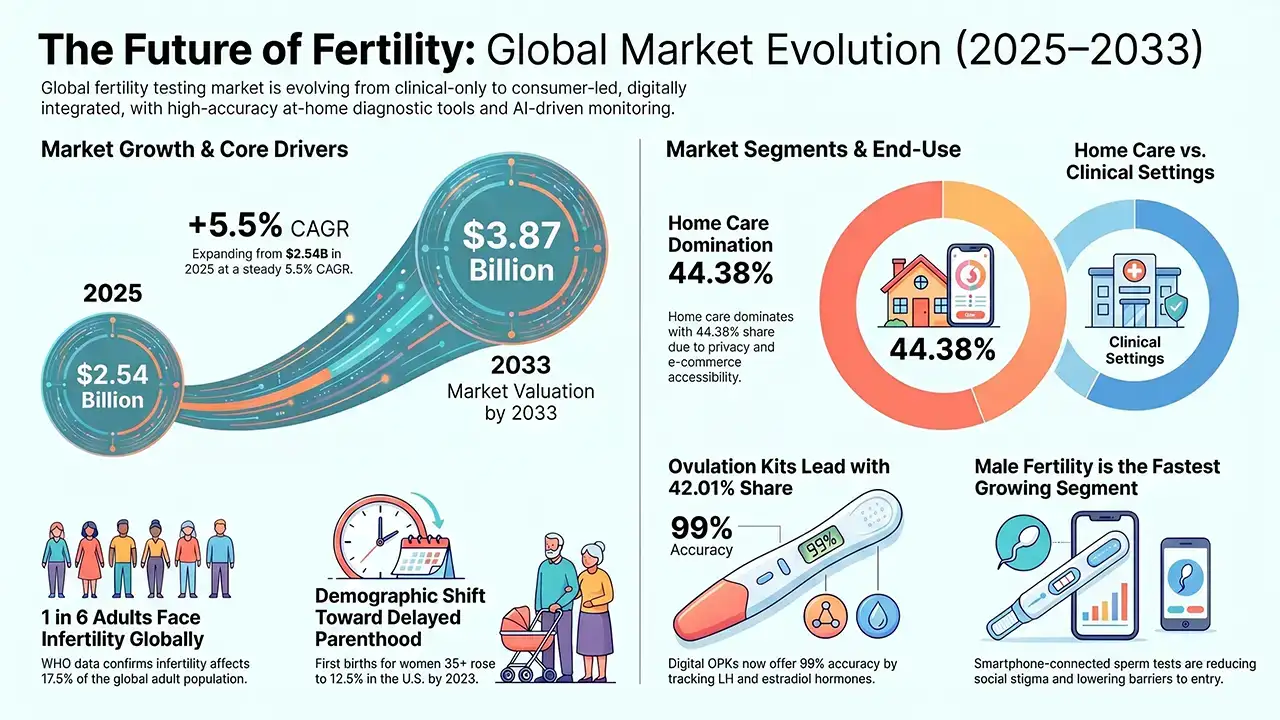

The global Fertility Testing Devices market, valued at USD 2.54 billion in 2025, is projected to reach USD 3.87 billion by 2033, growing at a CAGR of 5.5%. Rising infertility rates, delayed parenthood, and technology-driven at-home testing solutions are fueling robust worldwide demand across North America, Asia Pacific, and beyond.

Researchers at the Babraham Institute and Stanford University have engineered a 3D laboratory model of the human uterus to observe embryo implantation in unprecedented detail, up to day 14 of development. Published in Cell, this breakthrough opens new pathways for understanding IVF failure, miscarriage, and pregnancy complications.

Global fertility tourism is projected to reach US$13,080.0 Mn by 2032 at a 30.3% CAGR, led by IVF and a strong North America share.

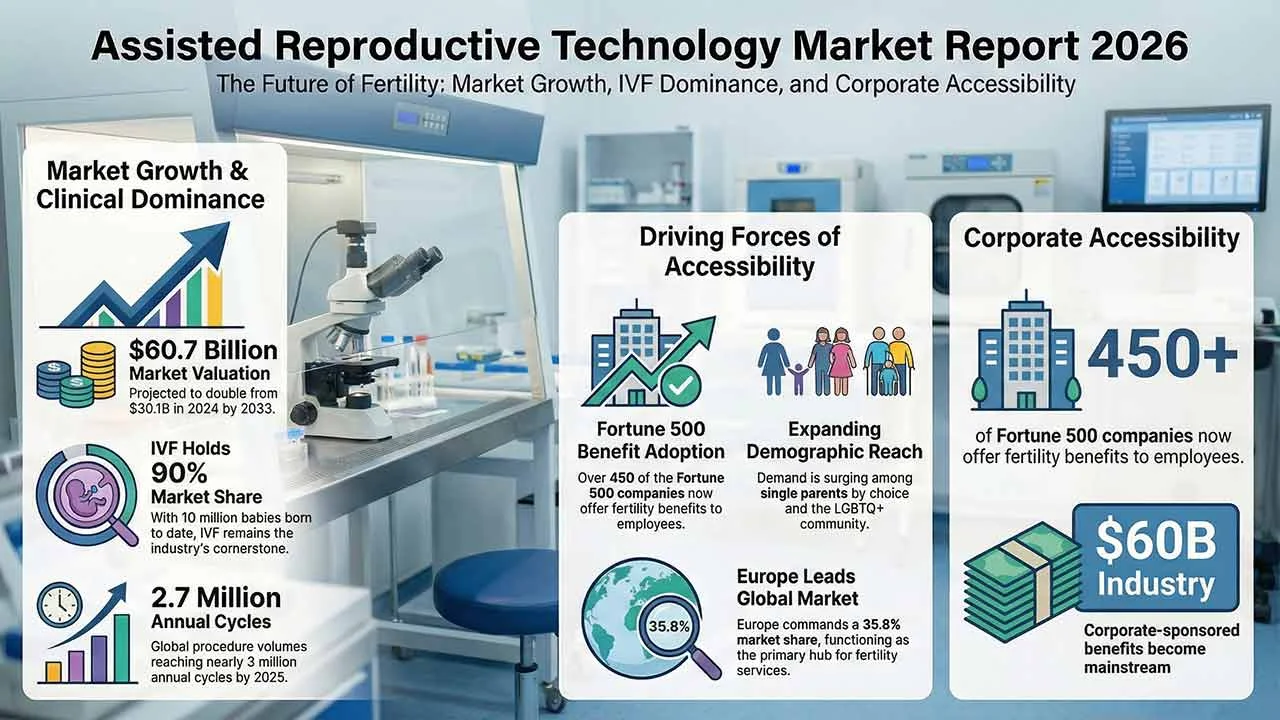

The assisted reproductive technology market continues to expand as infertility rates rise and parenthood is increasingly delayed worldwide. Valued at US$30.1 billion in 2024, the market is projected to reach US$60.7 billion by 2033, supported by IVF innovation, growing awareness, improved accessibility, and sustained investment in reproductive healthcare infrastructure globally.

The global human reproductive technology market is set to reach 45.4 USD billion by 2035, expanding from 27.7 USD billion in 2024 at a 4.6% CAGR. Growth is fueled by technological advancements in fertility treatments, rising infertility rates, delayed pregnancies, and increasing acceptance of single and LGBTQ+ parenting worldwide.

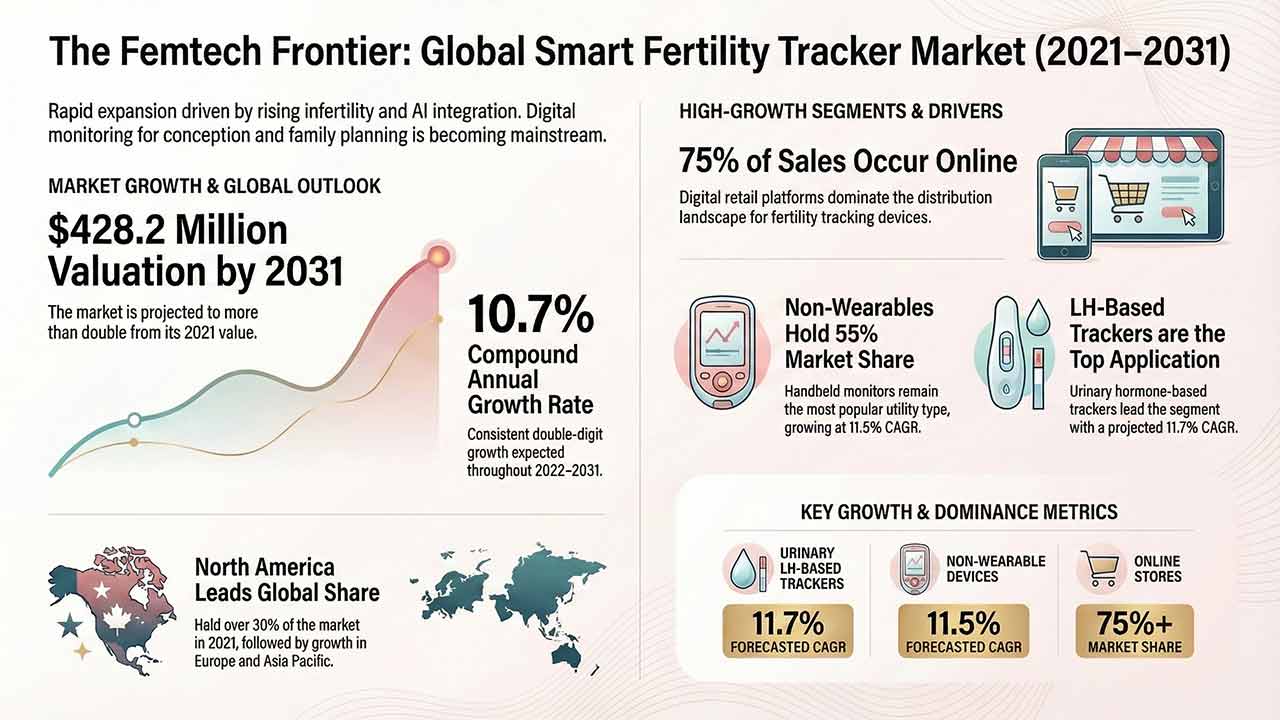

This comprehensive report analyses the Smart Fertility Tracker Market, detailing its projected growth from US$ 160.2 million in 2021 to US$ 428.2 million by 2031. It examines key drivers such as rising infertility and technological advancements in AI-integrated hormone monitoring, alongside detailed segmentation by utility, application, and region.

The Sperm Separation Systems Market is projected to exceed USD 1.5 billion by 2035, driven by automation, microfluidics, and rising male infertility awareness.