Home

ReportReport

ReportReportThis comprehensive analysis examines the global Donor Egg IVF market, forecasting a valuation of USD 5.7 billion by 2033. The report explores critical growth drivers, including delayed parenthood, technological breakthroughs in embryo selection, and shifting regulatory landscapes, offering a detailed breakdown of market segmentation and regional growth trajectories for the next decade.

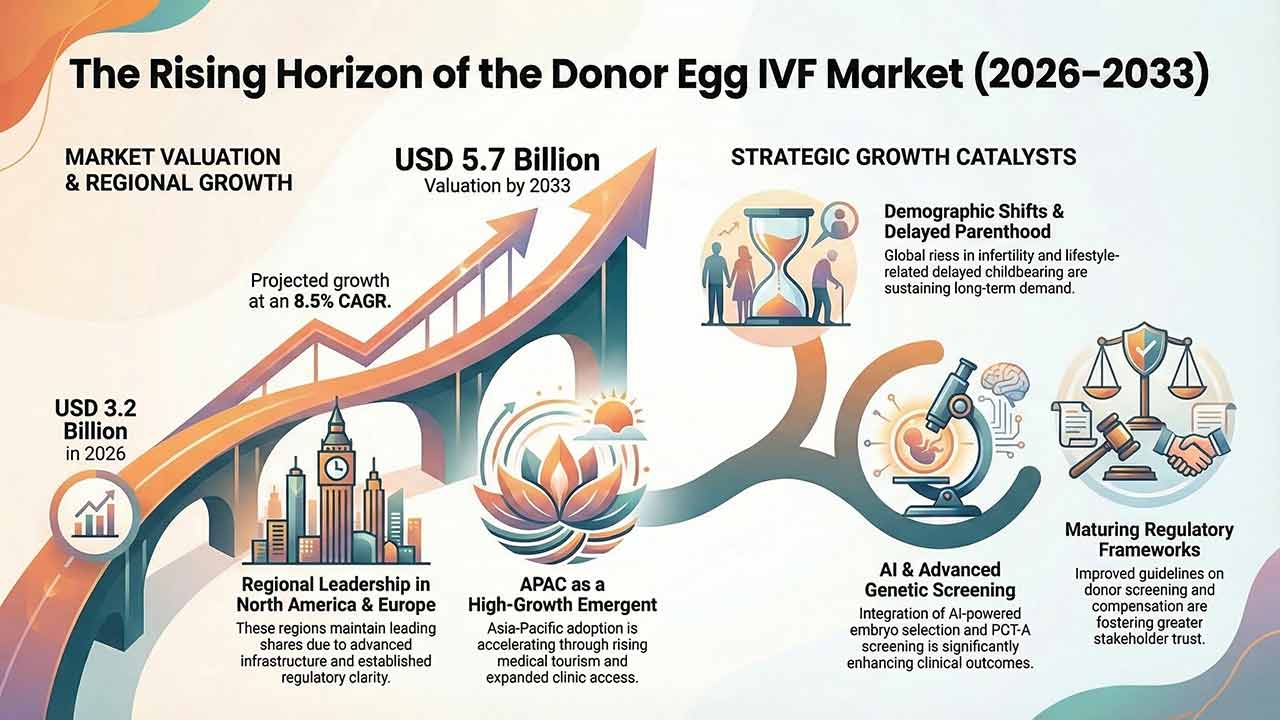

The Donor Egg IVF market is currently positioned as a critical segment within the broader assisted reproductive technology (ART) industry, addressing the complex needs of individuals and couples facing significant infertility challenges. As of 2026, the market is valued at approximately USD 3.2 billion and is on a robust upward trajectory. Industry forecasts suggest that the market will expand at a compound annual growth rate (CAGR) of 8.5%, ultimately reaching a total market size of USD 5.7 billion by the year 2033. This growth is being propelled by a combination of increasing global infertility rates, trends toward delayed parenthood, and rapidly evolving societal attitudes regarding third-party reproduction.

A primary structural catalyst for the expansion of the Donor Egg IVF market is the global rise in infertility rates. This increase is influenced by a variety of factors, including modern lifestyle changes, environmental stressors, and a notable increase in maternal age at the time of first conception. In many urbanised populations, there is a distinct societal shift toward delayed parenthood. This demographic trend has resulted in a higher proportion of the population requiring assisted reproductive solutions as natural fertility declines with age. Consequently, donor egg IVF procedures are increasingly seen as a core component of modern fertility care.

Technological innovation also serves as a major driver for market adoption. The integration of advanced laboratory techniques and improved cryopreservation methods has significantly enhanced the clinical success rates of these procedures. Furthermore, the normalisation of third-party reproduction has expanded the addressable patient base, as more individuals feel comfortable pursuing these options to build their families.

The market is witnessing a surge in value through the emergence of advanced genetic testing and screening technologies. Specifically, the integration of preimplantation genetic testing for aneuploidy (PGT-A) is creating new value pools within the landscape. These technologies allow for more precise embryo selection, which serves two critical functions: reducing the risk of inherited genetic disorders and improving overall live birth rates.

In addition to genetic screening, the adoption of time-lapse embryo imaging and other sophisticated laboratory standards is elevating patient expectations and clinical outcomes. Digital health platforms are also playing an increasingly vital role by facilitating patient education, streamlining the complex process of donor matching, and offering remote consultations. These digital tools are essential for expanding access to fertility services across different geographies. The convergence of data analytics and personalised medicine is further fostering tailored treatment protocols, which in turn drives higher patient satisfaction.

As the Donor Egg IVF market matures, regulatory frameworks are evolving to address complex ethical considerations and ensure the safety of all participants. Many regions are now implementing clearer, more stringent guidelines regarding donor screening and compensation. This maturation of the legal environment is fostering greater transparency and building trust among stakeholders, which is essential for long-term market stability.

However, ethical and regulatory complexities remain a notable constraint on adoption in certain jurisdictions. Inconsistencies in policies related to donor anonymity, privacy concerns, and compensation can create uncertainty for both healthcare providers and patients. Differing legal frameworks across international borders can also limit cross-border reproductive care, potentially slowing expansion in regions where regulations remain ambiguous or highly restrictive.

The market is characterised by several distinct segments that cater to the diverse needs of the patient population. These segments are categorised by the type of donor, the procedure used, the end-user, and the age of the recipient.

By Type of Donor:

By Procedure:

By Application:

By Age Group of Recipient:

By End User: The primary providers in the market include specialised fertility clinics, large-scale hospitals, and various research institutes that contribute to clinical developments.

The geographical distribution of the Donor Egg IVF market reflects the availability of advanced healthcare infrastructure and the level of regulatory clarity in different parts of the world.

The competitive landscape of the market consists of a mix of established fertility clinics, specialised assisted reproductive technology (ART) centres, and dedicated biobank providers. Participants in the market are increasingly focused on expanding their donor pools to offer more diversity and better matching options for patients. Strategic collaborations between fertility clinics and genetic testing providers are becoming common, as these partnerships allow for service differentiation and enhanced clinical outcomes.

Investments in laboratory technology and digital engagement tools are central to maintaining a competitive edge. By prioritising patient-centric solutions and adhering to evolving regulatory standards, providers can capture a larger share of the growing global patient base.

Looking ahead to 2033, the market is expected to remain a focal point for investment and clinical development. Its strategic relevance is underscored by its vital role in expanding reproductive options and supporting demographic sustainability in regions with declining birth rates. As healthcare systems worldwide increasingly prioritise patient-centric fertility solutions, the integration of data-driven protocols and advanced genetic screening will likely become the standard of care.

The transition toward USD 5.7 billion by 2033 reflects a fundamental shift in how society approaches family building. While challenges regarding ethical frameworks and cross-border legalities persist, the overall trajectory of the market is one of expansion, innovation, and increased accessibility. Stakeholders who successfully navigate the complexities of donor management, regulatory compliance, and technological integration will be best positioned to lead in this evolving landscape.

The University of Aberdeen has launched a redesigned, free IVF success calculator, the OPIS tool, powered by updated national HFEA data. Built with patients at its centre, the IVF success calculator provides tailored success estimates across up to six IVF or ICSI cycles, helping couples plan emotionally, physically, and financially.

A retrospective cross-sectional study of 276 ART patients suggests that the oestradiol-to-oocyte ratio (EOR) could serve as a meaningful prognostic marker for IVF outcomes in PMOS. The research examines EOR across four categories, incorporating subgroup analysis by luteinising hormone activity during ovarian stimulation.

AutoIVF's OvaReady device is advancing IVF egg retrieval technology by recovering "stealth oocytes" from discarded follicular fluid. With Northeastern University co-op students Tori Christianson and Jake Percival refining its prototypes, the Natick, Mass, based startup is preparing for clinical trials, aiming for FDA clearance to improve IVF success rates.

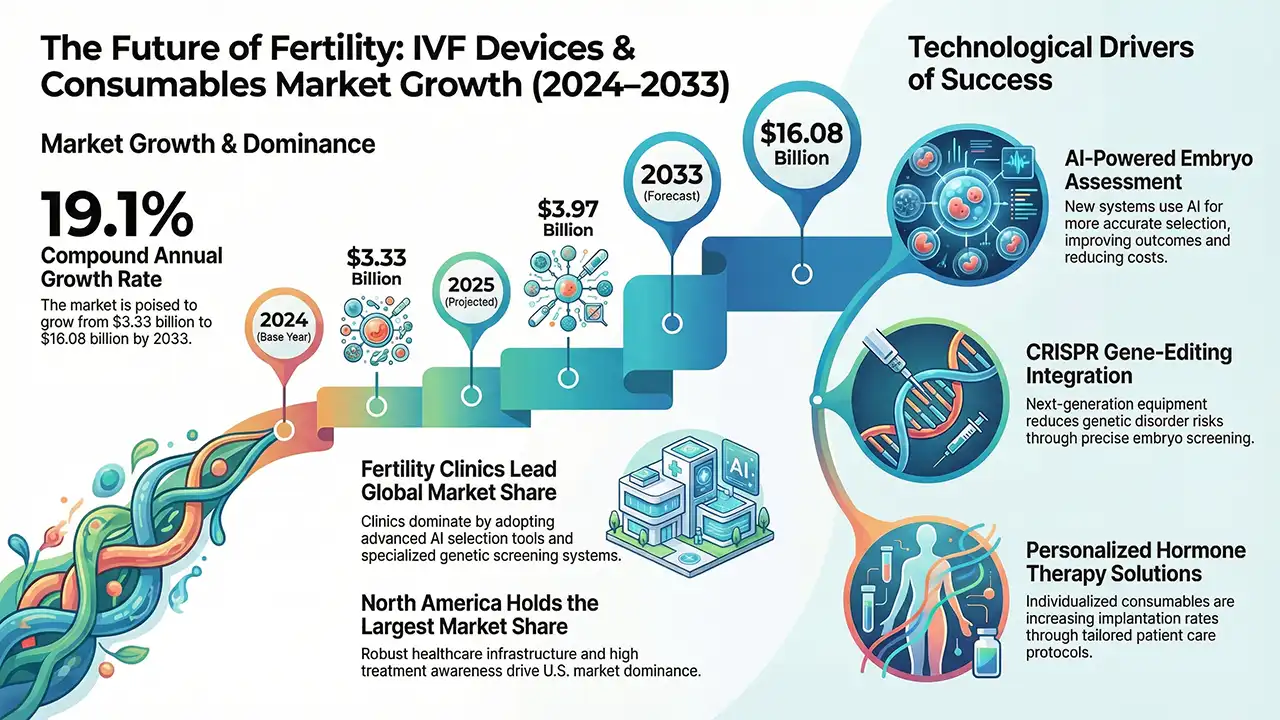

The global IVF Devices and Consumables market is projecting a significant surge to $16.08 billion by 2033. Driven by rising infertility and tech innovations, the analysis covers regional shifts, product segments, and emerging trends, highlighting the industry’s evolution alongside the growing Smart Fertility Tracker Market

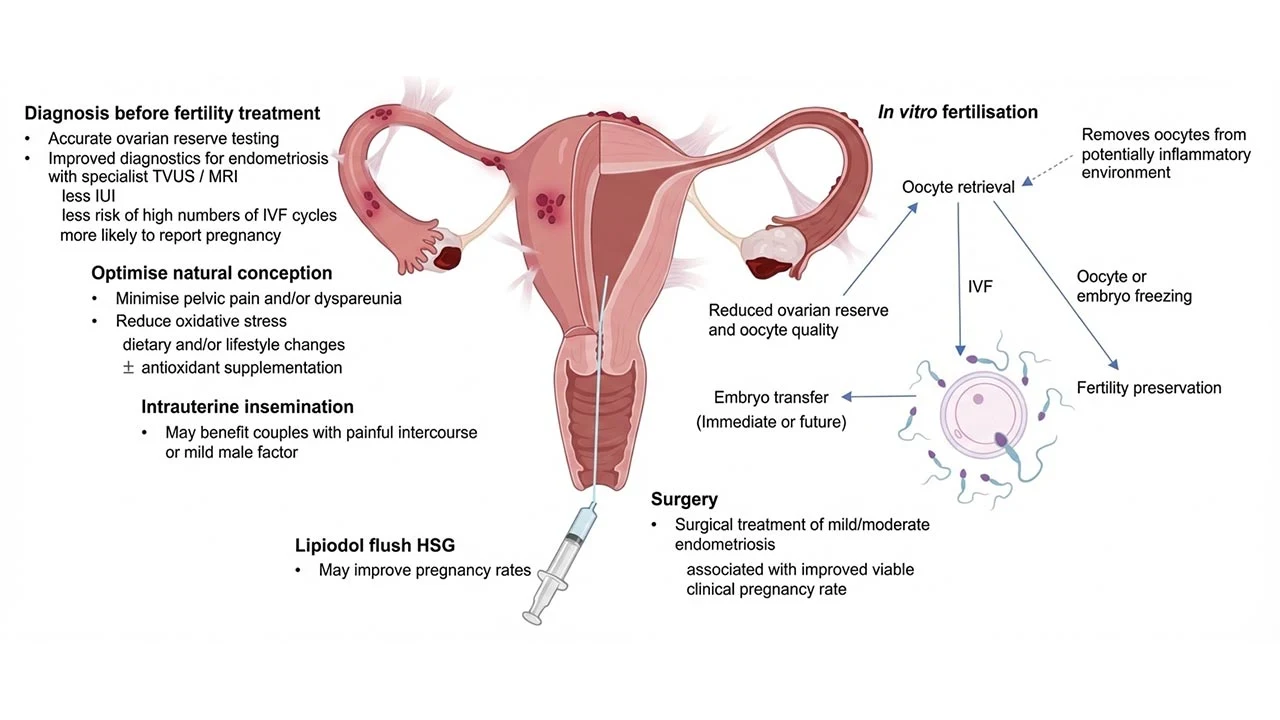

Integrating IVF and Surgical Management in Endometriosis offers a patient-centered strategy to improve fertility while managing chronic pain. By integrating laparoscopic surgery, ovarian reserve assessment, and assisted reproductive technology, clinicians can tailor treatment plans, enhance live birth rates, and optimize reproductive outcomes for women facing complex endometriosis-related infertility challenges.

Global Preimplantation genetic testing market outlook covering growth drivers, segmentation, regional trends, key technologies, restraints, opportunities, and competitive landscape approaching $1B by 2032.