Home

ReportReport

ReportReportThe global human reproductive technology market is set to reach 45.4 USD billion by 2035, expanding from 27.7 USD billion in 2024 at a 4.6% CAGR. Growth is fueled by technological advancements in fertility treatments, rising infertility rates, delayed pregnancies, and increasing acceptance of single and LGBTQ+ parenting worldwide.

The human reproductive technology market stands at a pivotal juncture of unprecedented growth and transformation. Projected to expand from 27.7 USD billion in 2024 to 45.4 USD billion by 2035, this dynamic sector demonstrates a steady compound annual growth rate of 4.6 percent throughout the forecast period from 2025 to 2035. This robust trajectory reflects the convergence of medical innovation, demographic shifts, and progressive social attitudes toward reproductive autonomy and diverse family structures.

The industry encompasses a comprehensive spectrum of medical interventions designed to address infertility and facilitate family planning, including in-vitro fertilization, surrogacy arrangements, sperm and egg donation programs, and advanced cryopreservation techniques. Rapid advancements in assisted reproductive techniques, coupled with escalating global infertility rates and the normalization of single and LGBTQ+ parenting, are fundamentally reshaping the fertility landscape. Strategic healthcare investments and increasingly favorable regulatory frameworks are providing additional momentum to this expanding sector.

The human reproductive technology market exhibits remarkable resilience and expansion potential as healthcare systems worldwide recognize reproductive medicine as essential care rather than elective treatment. Technological improvements in reproductive medicine serve as primary catalysts for market acceleration, enabling higher success rates and more accessible treatment pathways.

Several key factors underpin this growth trajectory. Lifestyle changes and delayed pregnancy decisions contribute significantly to rising infertility rates, particularly in developed economies where career prioritization and later-age family planning have become normative. Medical conditions including polycystic ovary syndrome and endometriosis, further expand the addressable patient population requiring assisted reproductive interventions.

The acceptance of diverse family structures represents another transformative driver. Single individuals now constitute a growing segment of market demand, supported by technological enablement and shifting social acceptance that validates non-traditional parenting pathways. LGBTQ+ individuals and couples similarly benefit from expanded access to reproductive technologies that make biological parenthood achievable regardless of traditional partnership models.

The human reproductive technology market research categorizes demand across multiple dimensions, providing granular insight into the ecosystem driving industry evolution. This segmentation framework encompasses intended parent type, gestational condition classifications, compensation structures, arrangement models, and legal frameworks that collectively shape market dynamics.

Infertile couples represent the largest demand segment, their numbers expanding due to lifestyle factors, postponed childbearing, and medical conditions that compromise natural conception. These couples often pursue multiple treatment cycles and advanced interventions, generating substantial recurring revenue within the fertility services sector.

Single individuals constitute a rapidly growing market segment, their participation enabled by evolving social acceptance and technological capabilities that separate reproduction from traditional partnership requirements. This demographic demonstrates strong purchasing power and determination, often pursuing premium service options including genetic screening and donor selection protocols that enhance treatment revenues.

The LGBTQ+ community represents an emerging high-value segment whose unique reproductive needs require specialized service configurations, including gestational surrogacy, gamete donation, and complex legal navigation. Their participation signals market maturation and the industry's evolution beyond heteronormative treatment paradigms.

Geographic distribution of the human reproductive technology market reflects disparate regulatory environments, cultural attitudes, and economic development levels that either facilitate or constrain service delivery. Developed markets including North America and Western Europe demonstrate high treatment penetration, sophisticated service offerings, and strong reimbursement frameworks that support market expansion.

Emerging markets present substantial growth opportunities as healthcare infrastructure modernizes, disposable incomes rise, and cultural attitudes toward assisted reproduction liberalize. These regions often experience rapid market acceleration once regulatory clarity emerges and quality service providers establish operations.

The competitive landscape features specialized fertility clinics, hospital-based reproductive medicine departments, and integrated service providers offering comprehensive treatment pathways. Technology companies supplying laboratory equipment, genetic testing platforms, and embryology systems constitute essential ecosystem participants whose innovations drive clinical outcomes and operational efficiencies.

Cutting-edge developments in reproductive medicine continuously expand treatment possibilities and success probabilities. Advanced embryo selection techniques utilizing artificial intelligence and genetic screening technologies enable clinicians to identify optimal transfer candidates, improving implantation rates and reducing cycle requirements.

Cryopreservation technologies have matured substantially, with vitrification protocols delivering survival rates exceeding 95 percent for frozen embryos and oocytes. This capability empowers fertility preservation for medical reasons, enables treatment timing flexibility, and supports donor programs with expanded inventory management.

Laboratory automation and quality management systems enhance consistency, reduce human error, and improve operational scalability for high-volume fertility centers. These technological investments deliver compound benefits through enhanced success rates, reduced complications, and superior patient experiences that drive referral patterns and market share gains.

Despite robust growth projections, the human reproductive technology market confronts meaningful headwinds including cost barriers that limit treatment access for middle-income populations without insurance coverage or subsidy programs. Treatment cycles frequently require multiple attempts, creating cumulative financial burdens that exclude substantial portions of the addressable patient population.

Regulatory fragmentation across jurisdictions creates operational complexity for providers and confusion for patients seeking treatment options. Varying legal frameworks governing surrogacy, donor anonymity, embryo disposition, and permissible techniques require sophisticated compliance infrastructure and limit cross-border treatment coordination.

Ethical considerations surrounding genetic selection, embryo research, and commercial surrogacy generate ongoing debates that influence regulatory evolution and social acceptance. Industry participants must navigate these sensitive discussions while maintaining operational viability and protecting patient interests.

The trajectory toward 45.4 USD billion market valuation by 2035 reflects not merely a continuation of existing trends but acceleration driven by converging catalysts. Healthcare systems increasingly recognize infertility as a medical condition warranting coverage parity with other diagnoses, expanding reimbursement frameworks that reduce patient cost barriers.

Technological convergence between reproductive medicine, genomics, and artificial intelligence promises breakthrough innovations that dramatically improve success rates while reducing treatment burdens. These advances position the human reproductive technology market for sustained expansion beyond current forecast horizons.

Strategic opportunities abound for providers who develop integrated service models addressing the complete patient journey from diagnosis through successful pregnancy and beyond. Value-based care frameworks, outcomes guarantees, and financing innovations can expand market access while maintaining provider economics.

The human reproductive technology market demonstrates exceptional growth potential supported by demographic imperatives, technological innovation, and social evolution. The expansion from 27.7 USD billion in 2024 to 45.4 USD billion by 2035 at a 4.6 percent compound annual growth rate reflects fundamental shifts in how societies address infertility and enable diverse family formation.

Industry participants positioned at the intersection of clinical excellence, technological sophistication, and patient-centered service delivery will capture disproportionate value as this market matures. The convergence of medical capability and social acceptance creates unprecedented opportunities for organizations committed to expanding reproductive autonomy and delivering successful outcomes for all patients seeking to build families.

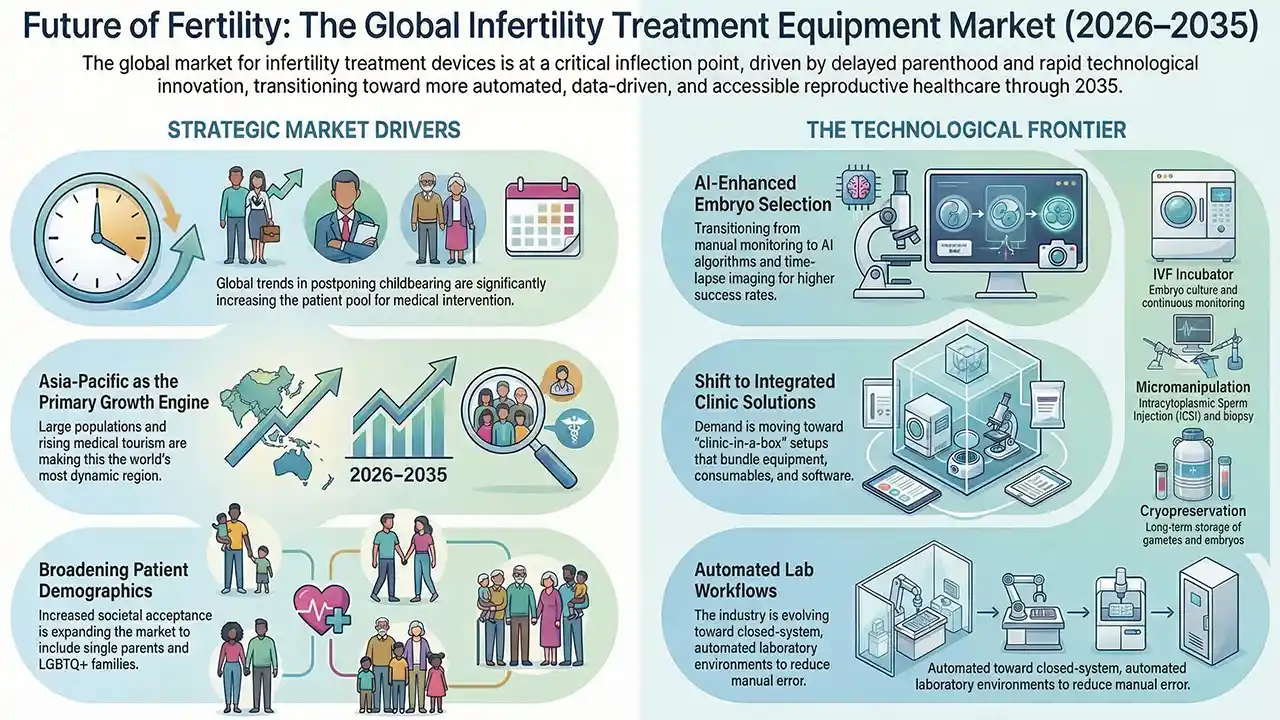

An analysis of the global infertility treatment devices and equipment industry through 2035. It examines critical market drivers such as delayed childbearing, technological innovations in AI and automation, and regional growth patterns, offering strategic insights into the evolving landscape of assisted reproductive technology worldwide.

Human preimplantation embryo arrest in ART remains a major challenge in IVF, affecting early embryo development and success rates. Driven by genetic mutations, epigenetic disruptions, and metabolic failures, this condition halts growth before implantation, prompting advances in AI-based embryo selection and precision medicine to improve reproductive outcomes.

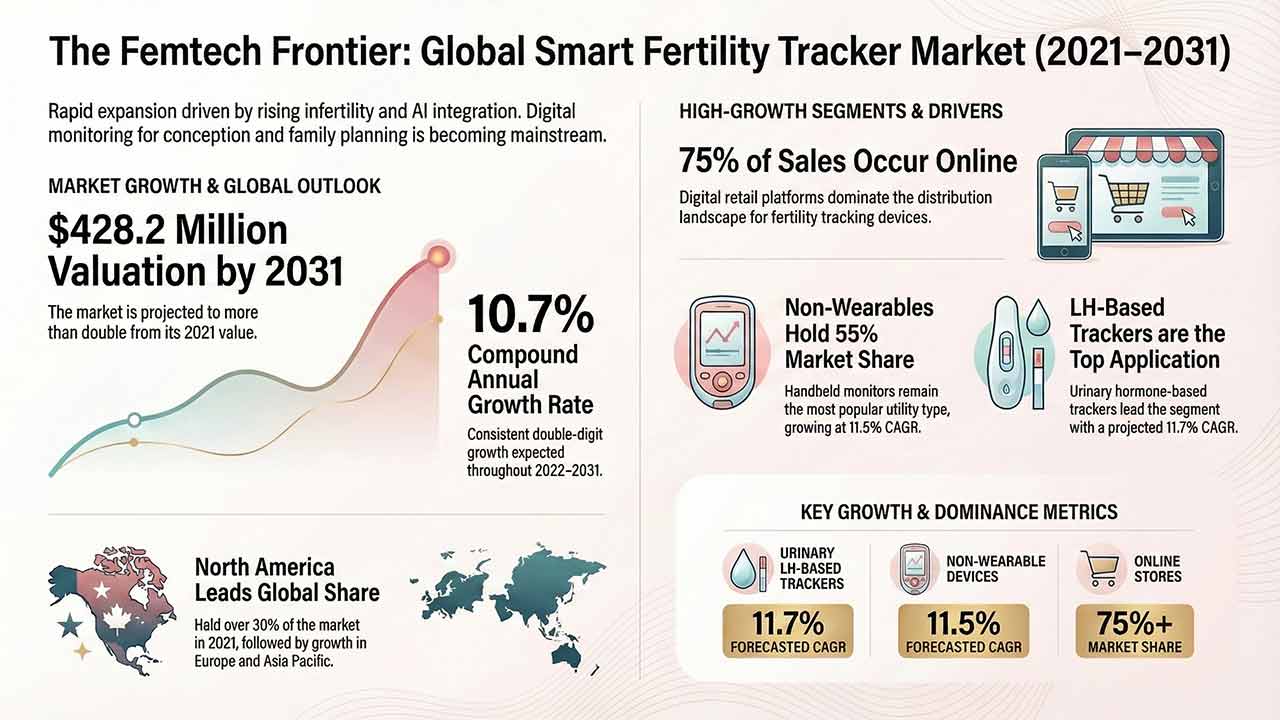

This comprehensive report analyses the Smart Fertility Tracker Market, detailing its projected growth from US$ 160.2 million in 2021 to US$ 428.2 million by 2031. It examines key drivers such as rising infertility and technological advancements in AI-integrated hormone monitoring, alongside detailed segmentation by utility, application, and region.

Gen Z women fertility awareness is marked by high anxiety but limited clinical knowledge, according to new ASRM-published research. While most young women want children, many misunderstand IVF success rates, miscarriage risks, and age-related decline, highlighting an urgent need for proactive, evidence-based reproductive education initiatives.

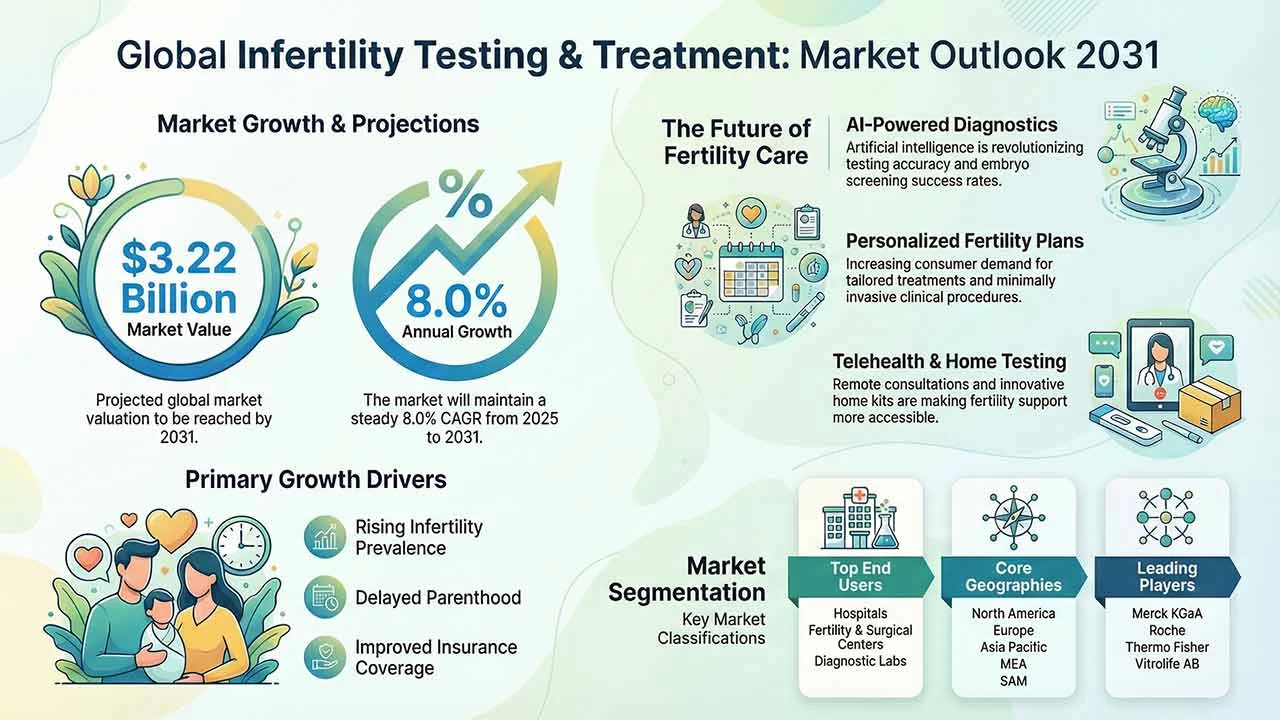

The global infertility testing and treatment market is projected to reach US$3.22 billion by 2031, expanding at an 8% CAGR. Growth is fueled by delayed parenthood, rising infertility rates, AI-driven diagnostics, advanced ART procedures, and expanding healthcare access across North America, Europe, and Asia-Pacific regions.

Market analysis of the infertility drugs market, highlighting the dominance of gonadotropins, online pharmacies as key channels, the competitive landscape, and regional trends, with insights and infographics for 2025-2032.

The Human Reproductive Technologies market is poised for steady growth through 2032, driven by strategic moves from leading players, segmentation expansion, and region-specific demand shifts.